**The following text and slides are from a lecture by Adair Turner at the British Institute of Energy Economics ‘Future of Energy Lecture 2024’ – presented on May 16th 2024.**

Economic consequences of a net-zero economy: investing for a better future

It is 10 years since the start of this lecture series and 16 years since the UK Climate Change Committee was established in 2008. So I’d like this evening to ask what we have learnt over the last 10-15 years about the economics of achieving an energy transition to a zero carbon economy.

One thing to remember is that in 2008, when the CCC was established, there was no clear intention, either in Britain or globally, to achieve a net-zero carbon economy. The UK Climate Change Act of 2006 committed the UK to achieving a 60% reduction in emissions by 2050: the CCC in 2008 recommended that the target should be 80%: and it was only in 2019 that the UK committed to achieving net-zero emissions by 2050.

At the Energy Transitions Commission we now believe that all developed economies should commit to reach net-zero emissions by 2050 at the latest, and all developing economies by 2060 at the latest. And across the word most countries are now committed to that principle, including crucially China, with its 2060 net-zero goal.

That increasing global ambition has reflected increasing recognition that climate change is occurring quite as fast as – and perhaps a bit faster than climate models predicted, and is already having serious adverse effects on human welfare across the world.

The IPCCs 2018 report warned that if global average temperatures rose more than 1.5°C above the industrial levels, severe adverse effects would occur and increase with every 0.1°C by which we overshot that limit. But over the last 12 months the global temperature has been 1.61°C above pre- industrial levels, and massive floods in Brazil, and heat waves in India and Indonesia are signs that the dangers of which the IPCC warned are already here.

We have set more stretching emission reduction targets because we face red flashing lights telling us we must.

But so far, higher ambition has not been matched by emissions reductions at the global level. Over the last 15 years indeed, global GHG emissions have increased from 46.8 – 53.8 GT (2007 to 2022) as Chinese emissions have grown by 58%, while developed economy emissions have only slowly reduced.

So we have rising ambitions, but still rising emissions, rising temperatures, and increasing adverse effects – quite a gloomy start to this lecture.

But the good news is that over the last 10-15 years technological progress and cost reductions has made it possible to decarbonise the energy, building industry and transport systems far more rapidly, more deeply and at much lower cost than we dared hope 16 years ago. These trends indeed make it now inevitable that by sometime in the second half of the 21st century we will have a close to net-zero global economy and that once we get there, the impact on conventionally measured living standards will be either trivial or a positive one – while the benefits of reducing the degree of global warming will be huge.

But that still leaves us facing big challenges and significant economic costs if we are to get there fast enough.

So in this lecture, I will both describe the attainable end point and the economic challenge – which is essentially an investment challenge – of getting there.

Technological progress and cost reduction

Slide 1

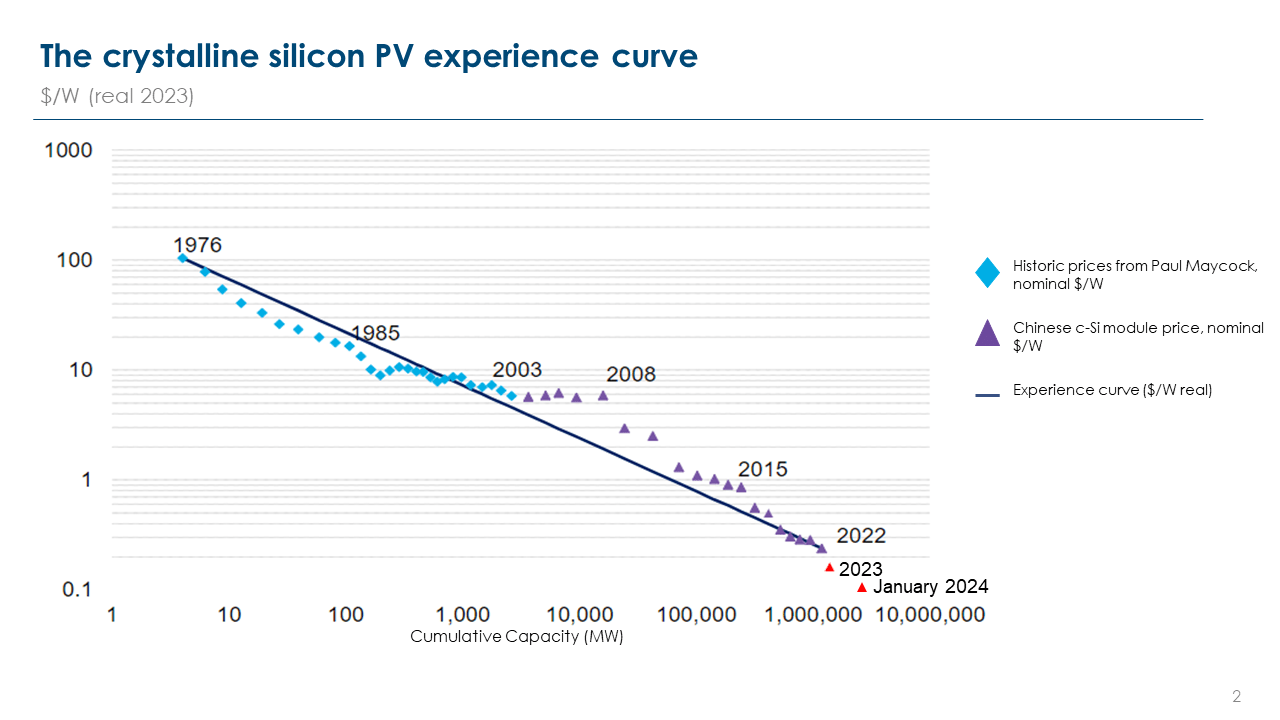

Over the last 50 years the price of solar PV per watt has fallen not 90%, not 99%, but 99.89%, from $100 per watt in 1974 to $.11cents per watt available from Chinese manufacturers today (Slide 1). Even after shipping costs and retailer margins, the price can be below $20 cents per watt, as in this Spanish supermarket (Slide 2). And further significant reductions in cost and increases in efficiency are inevitable.

Slide 2

Over the last 50 years the price of solar PV per watt has fallen not 90%, not 99%, but 99.89%, from $100 per watt in 1974 to $.11cents per watt available from Chinese manufacturers today (Slide 1). Even after shipping costs and retailer margins, the price can be below $20 cents per watt, as in this Spanish supermarket (Slide 2). And further significant reductions in cost and increases in efficiency are inevitable.

Over the last 50 years the price of solar PV per watt has fallen not 90%, not 99%, but 99.89%, from $100 per watt in 1974 to $.11cents per watt available from Chinese manufacturers today (Slide 1). Even after shipping costs and retailer margins, the price can be below $20 cents per watt, as in this Spanish supermarket (Slide 2). And further significant reductions in cost and increases in efficiency are inevitable.

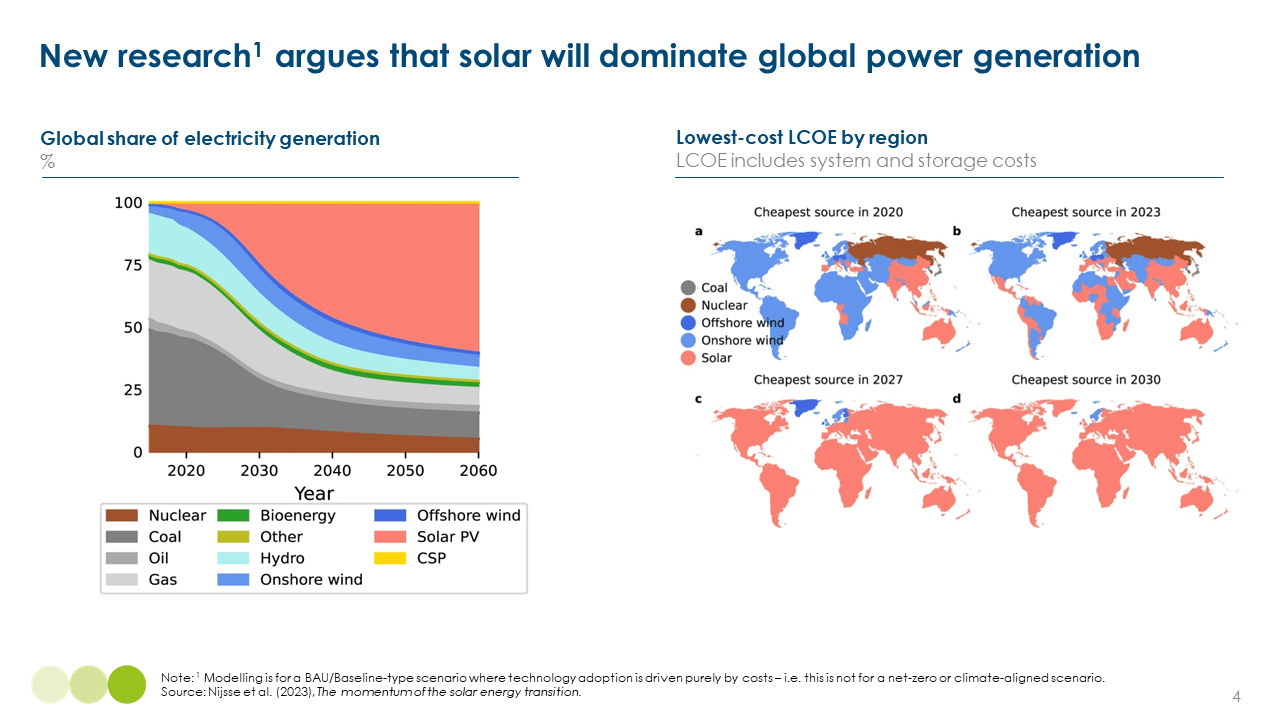

By 2008, a 90 % reduction had already occurred, and at the CCC we knew costs would continue to come down, but we were bluntly useless at foreseeing what would occur. We assumed a cost reduction of 20% by 2020; in fact costs fell by 85%. In 2008 I had a hunch that solar PV might become the cheapest electricity source in the second half of the 20th century: but no idea that credible analysis would show that it is already the cheapest way to produce a kwh of electricity generation across most of the world (Slide 3).

Slide 3

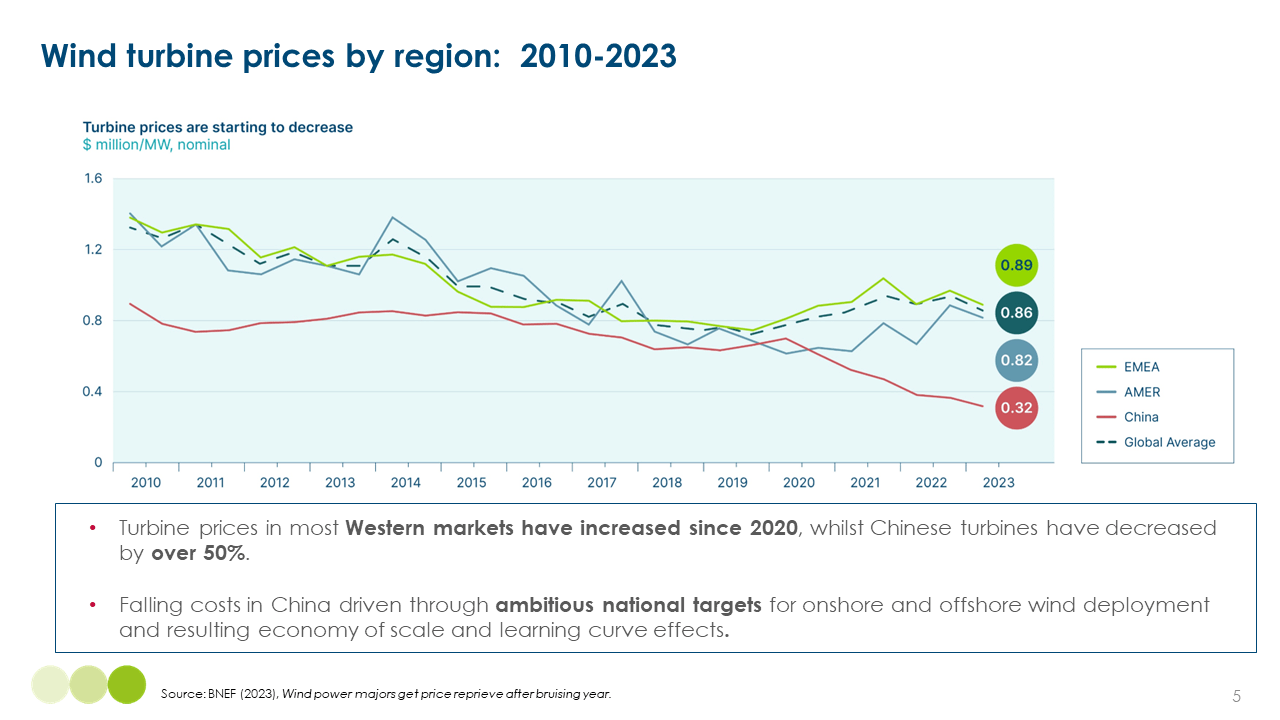

We also knew at the CCC, that the UK’s offshore wind resource was huge, and might become economic if costs could be reduced from the £150 per megawatt hour assumed in 2008. So in 2015, the CCC analysed what technological development, policy support, and supply chain development could get UK costs below £100 per megawatt hour by 2020. But in 2020 the winning bid in the fourth round of auctions was £39 per hour, and even after significant increases in the last few years, UK offshore wind is available at about £55 per MWh. Meanwhile, onshore wind costs have fallen by about 60% across the world between 2010 and 2020: and wind turbine prices in China have come down by 40% in just the last two years (Slide 4).

Slide 4

Slide 5

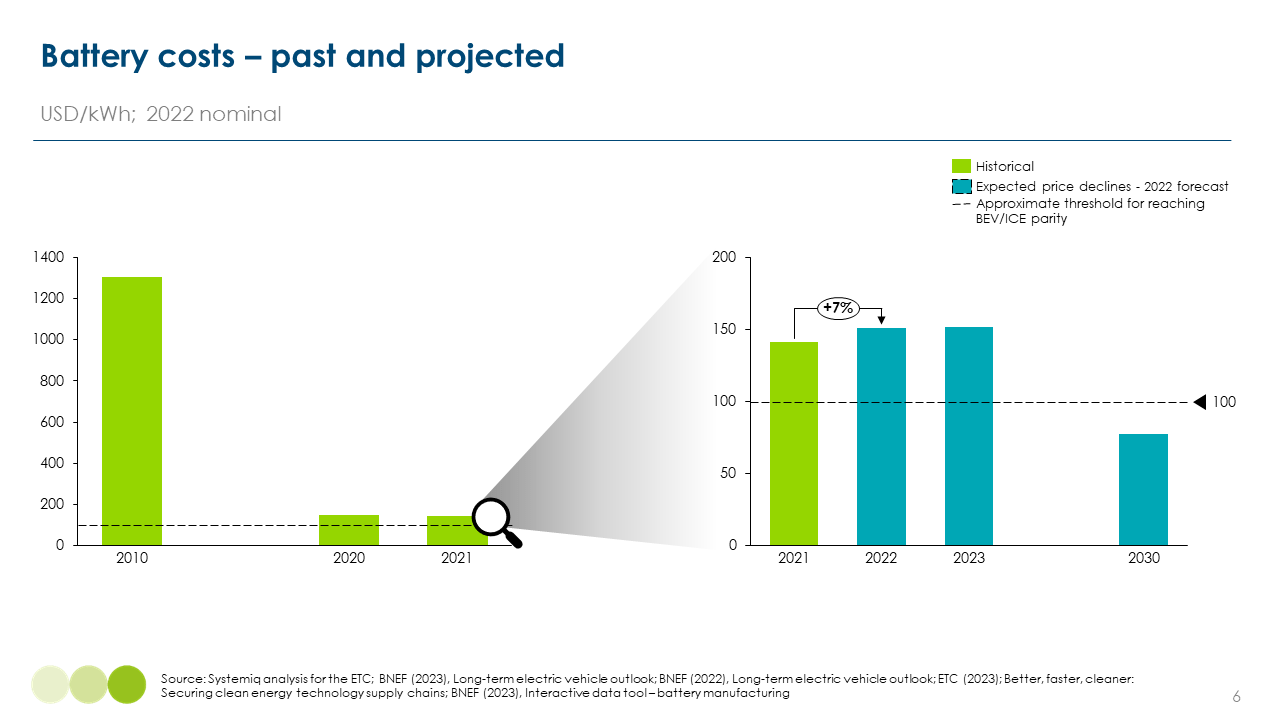

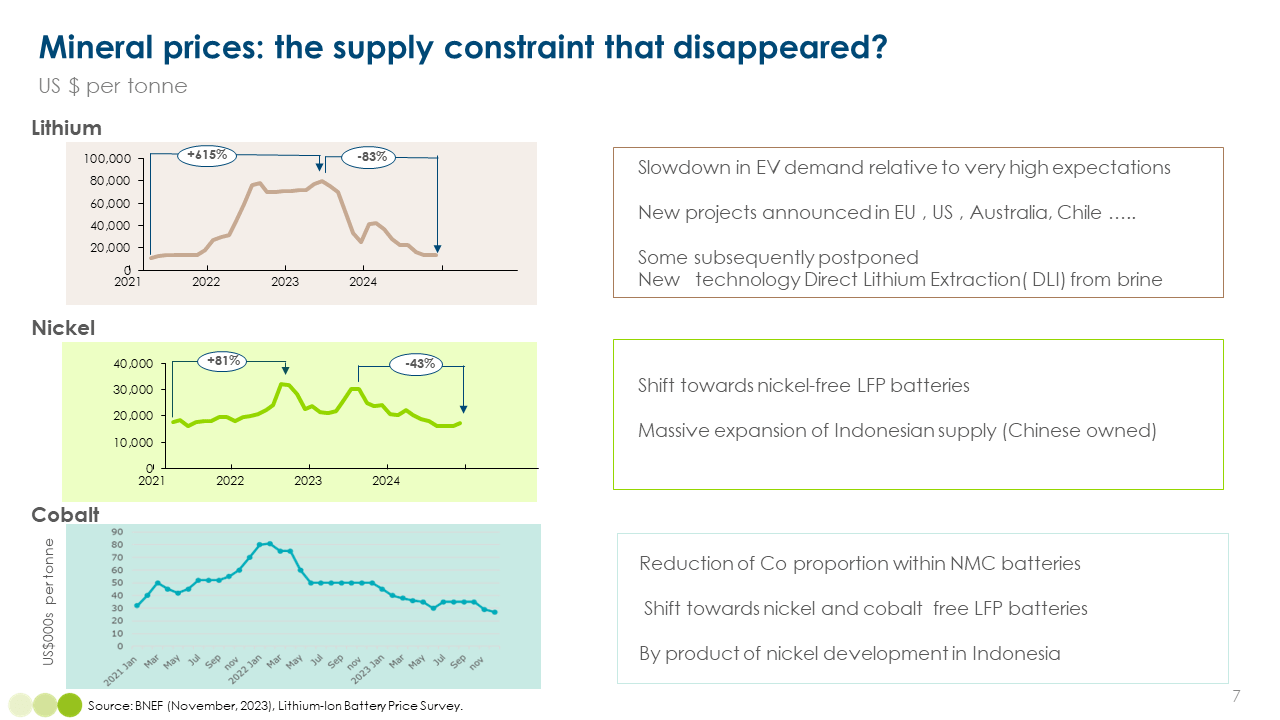

The cost of batteries has also collapsed. In 2010, the US Department of Energy set a target to reduce lithium ion battery costs from $1000 per kilowatt hour to $200 by 2020. But when 2020 came round, EV batteries were available for less than $130 per kilowatt (Slide 5). From 2021 to 2023 cost reduction stalled because of rising mineral input costs – nickel, cobalt and lithium prices up between 3 and 5 times; but these increases have now entirely reversed, and battery costs have resumed their downward path (Slide 6).

Slide 6

Technological progress indeed, through the development of LFP (lithium ferrous phosphate) batteries has made it possible to produce batteries which have no nickel or cobalt requirement; and lithium supplies are expanding fast.

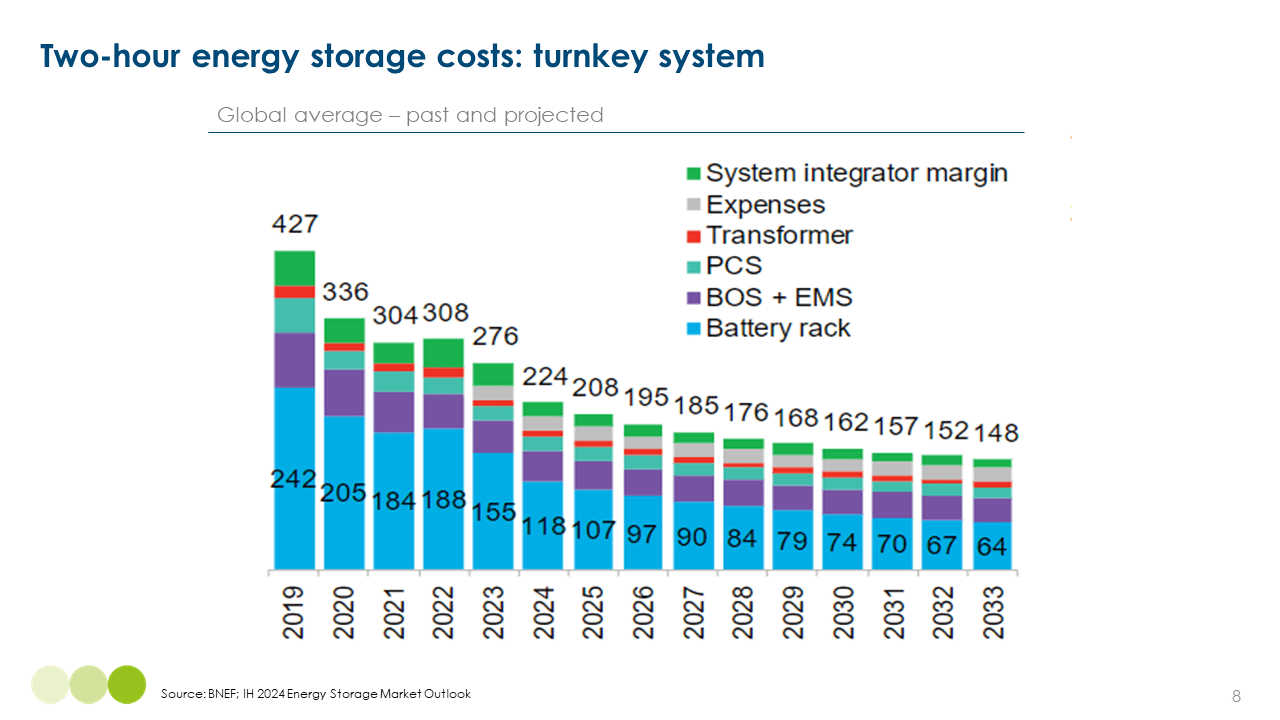

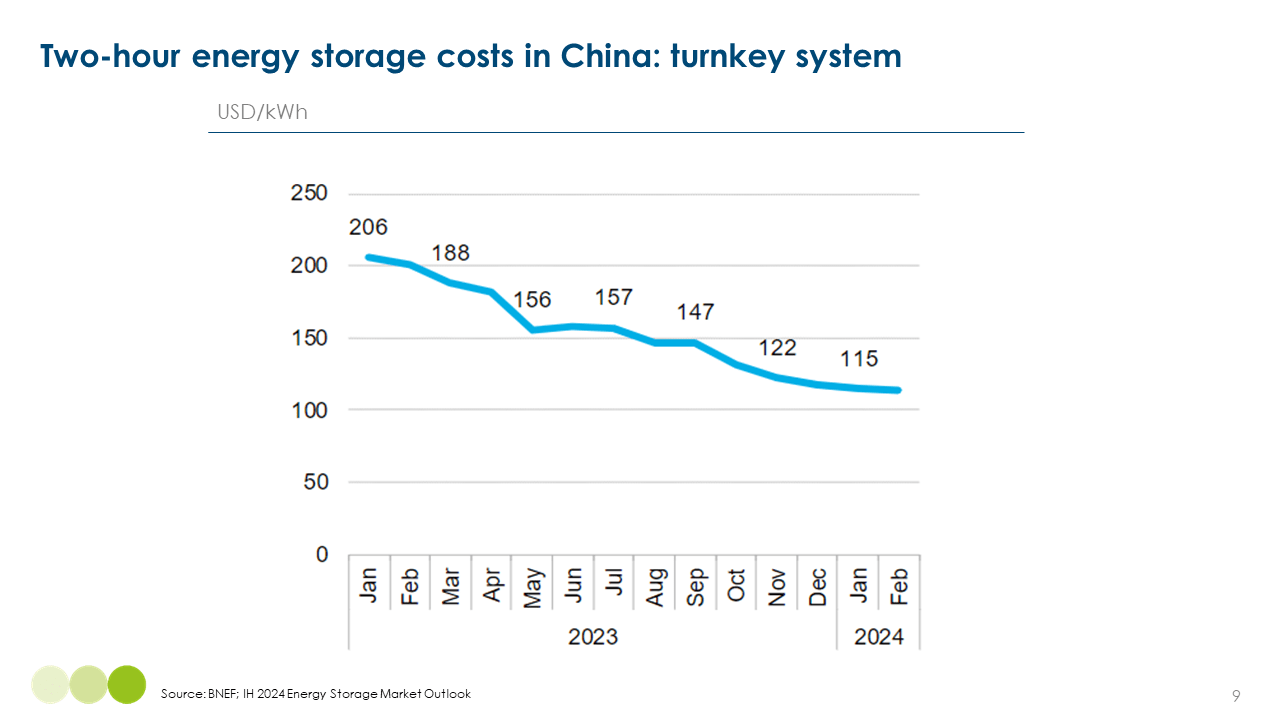

Not only as result are EV battery costs falling again, but also the cost of batteries for energy storage. BNEF estimate that the cost for complete systems could fall from $240 per kilowatt hour today to $148 by 2033: but in China, you can already purchase complete systems at $115 per kilowatt hour (Slide 7 and 8).

Slide 7

Slide 8

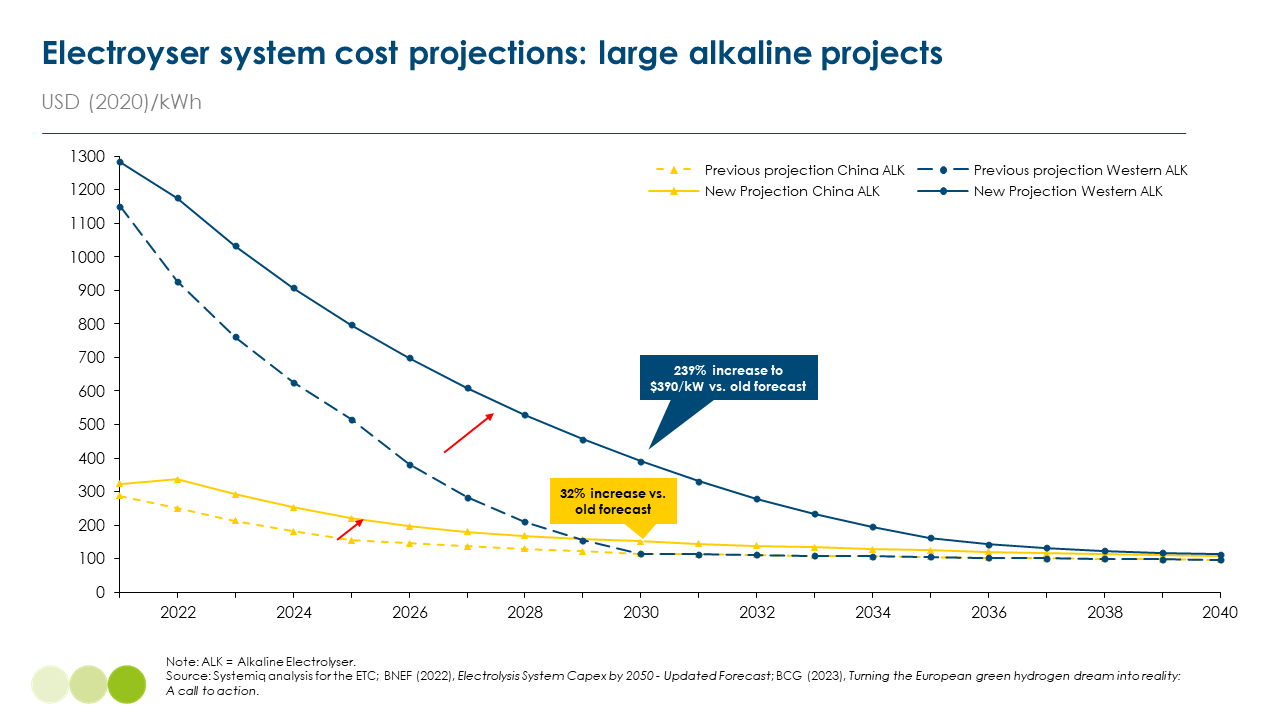

Other crucial technologies are also making progress and have the potential to achieve far more. The cost of electrolysers to produce green hydrogen has not yet fallen in the US and Europe at the pace which some commentators believed five years ago. But China’s far lower total system cost – at about $300 per kilowatt versus $800 per kilowatt in Europe – shows that dramatic cost reduction is technologically possible (Slide 9).

Slide 9

Heat pump technology (which is the key to both electrified heating and air-conditioning) is also progressing rapidly: achievable coefficients of performance could rise from today’s typical 4 to as high as 8; and high temperature heat pumps will make it increasingly possible to electrify residential homes without as much expenditure on improved insulation as we used to assume was needed.

Bring all of these technologies together, and the path to a net-zero economy, in Britain and globally, is far clearer than it was 10 to 15 years ago. The essence of what we must do is simple;

- Decarbonise electricity systems as fast as possible primarily with renewables.

- And electrify as much of the economy as possible.

In decarbonising electricity systems the biggest challenge is no longer how to generate a cheap hour of zero-carbon electricity – in most of the world the answer is simple and is either wind or solar. The challenge instead is what to do when the wind doesn’t blow or the wind doesn’t shine – how to balance demand and supply in systems dominated by variable renewables. But the technologies to do that cost effectively are now available.

Across many of the most populated, rapidly growing and hotter countries of the world – where solar is likely to be the dominant generation source, and where the main balancing challenge is from day to night, batteries will be an increasingly economic solution.

In less sunny but quite often windy northern climates, the biggest challenge will be seasonal – what to do when a winter anticyclone produces both high heating demand and minimal wind. But it is clear that solutions are available;

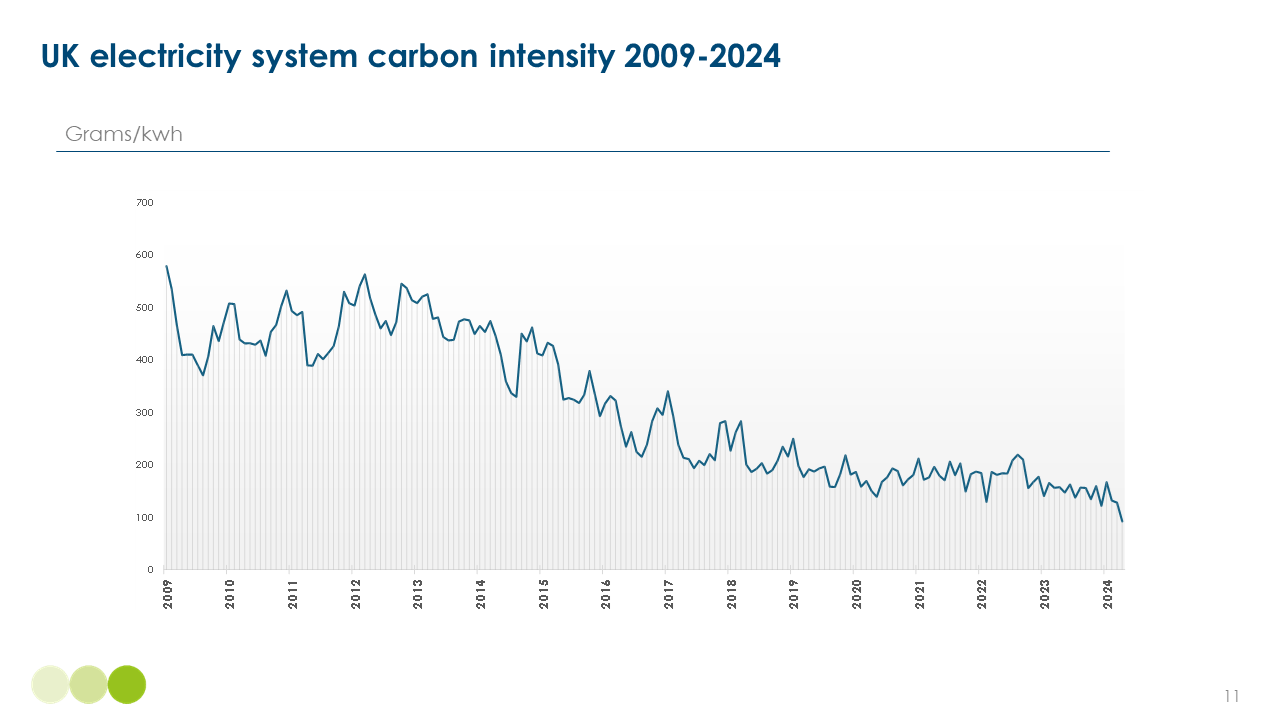

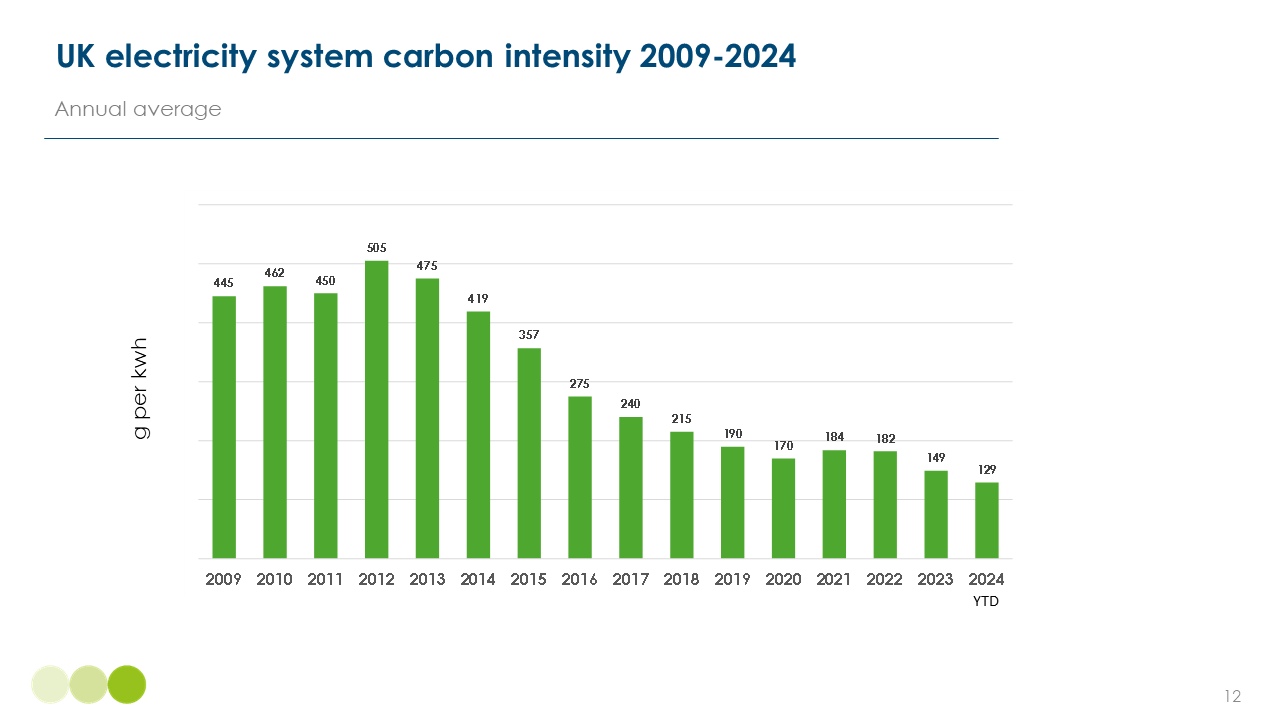

- Since 2010 the UK has already reduced the carbon electricity of its electricity from 500g per kwh in the first 17 weeks of the year to just 120g per kwh in the same weeks in 2024 – and that has been achieved with minimal deployment of batteries and none of H2 storage, simply by running gas plants on a flexible basis to offset variations in renewable supply (Slide 10 and 11).

- And analysis from the CCC’s Sixth Carbon Budget assessment shows that the UK power system could be producing twice as much electricity in 2050 based on 80% wind and solar resources at a total system cost per kwh no higher than today.

Slide 10

Slide 11

Analysis by the ETC and others from across the world confirms that conclusion; by 2050 “round the clock” zero-carbon electricity could be available at costs very similar to, and in some cases below, today’s fossil fuel based electricity.

And with clean electricity, batteries and heat pumps, and other application technology, we can electrify most of our economies. Today electricity only accounts for about 20% of final energy demand: but in China that is already approaching 30%, and everywhere it will rise fast. The IEA ‘s Net Zero scenario suggested that by 2050, it will reach almost 55%; but at the Energy Transitions Commission we believe it might be significantly higher at 65% – and each time we look again of the potential role of electricity versus other technologies, we tend to increase our estimated share, with for instance greater opportunity to electrify industrial heat, whether at medium temperatures of say 200 to 400°C or at high levels up to 1000°C – than we anticipated only five years ago.

It is important moreover to recognise that estimates of the percentage of final energy demand provided by electricity, significantly under state the importance of electricity in providing energy services, simply because electricity applications are so much more efficient.

If, for instance in 2040, 80% of the European passenger car fleet is EVs and 80% of all the kinetic energy used in passenger cars derives from electricity, rather from gasoline or diesel, our standard measure of final energy demand – which measures the energy content of the gasoline or electricity that we put into the car – will still say that only 50% of energy demand is for electricity. This is because when you use an ICE roughly 75% of all the energy you put in gets wasted as heat.

Similarly in residential and commercial building heating, when we switch from gas boilers to heat pumps, we go from systems which are at most 90% efficient in turning input energy into usable heat within the home, to ones that can be 400% efficient today and potentially much higher in future.

We sometimes talk of clean energy supply and of energy efficiency improvements as two different routes to decarbonisation – but the biggest driver of energy efficiency improvement over the next 30 years will be electrification itself.

The combined effect of the collapsing cost of renewable energy and batteries, and the inherently greater efficiency of electrified applications, means that in many areas of the economy the costs facing consumers in a zero-carbon economy will be below those faced when our energy is derived from fossil fuels.

Household will in future pay less to heat their homes with heat pumps than they currently do when they use gas boilers: and passenger car drivers and freight truck owners will pay less for electricity than they do today for gas and diesel. Indeed in the case of passenger cars, they will also soon pay less upfront as well.

- Complex ICE engines and drive trains are inherently more expensive than simpler electric engines.

- Conversely, EVs need expensive batteries instead of relatively cheap fuel tanks.

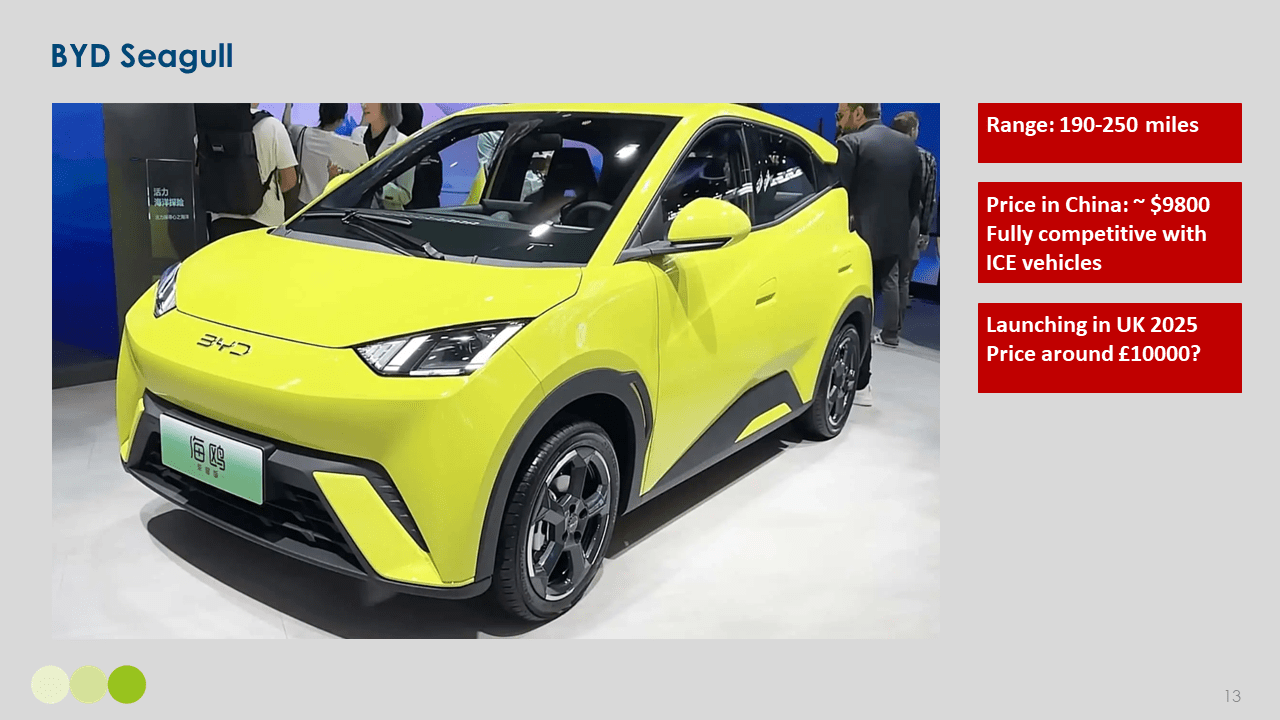

But once batteries get cheap enough, EVs will be cheaper than ICE vehicles. That crossover probably occurs when batteries go below around $100 per kwh, and in China it looks as if that crossover has already occurred; no ICE is likely to beat the quality and performance of the BYD Seagull priced at $11000 (Slide 12).

Slide 12

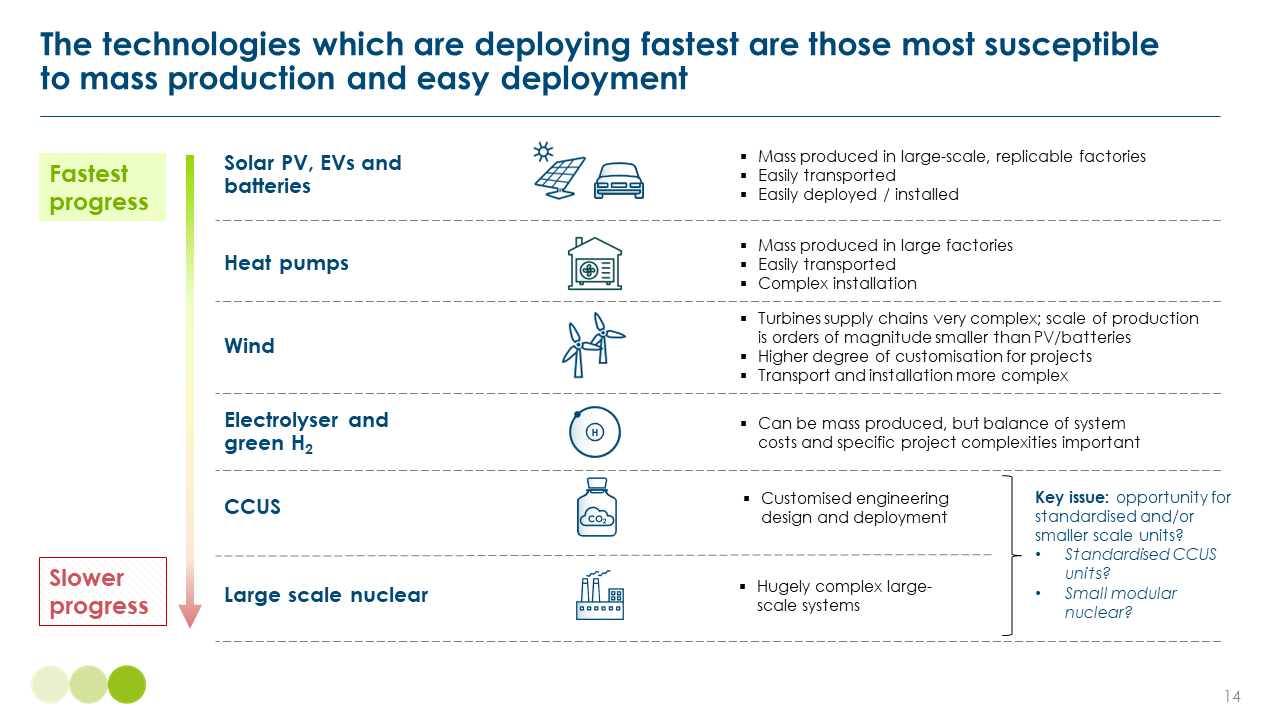

But not all technologies are falling in cost as fast as solar panels, wind turbines or batteries. Since 2008 solar PV costs have come down far faster than the CCC assumed. But estimated costs for carbon capture have stayed pretty much as we then estimated; and the estimated costs of new nuclear power are significantly higher than we then assumed. A clear pattern has emerged (Slide 13):

- Costs have fallen most rapidly in technologies which entail huge scale production of standardised components and products – millions of standardised solar cells assembled into tens of millions of standardised solar panels, hundreds of millions of standardised battery cells assembled into millions of standardised battery modules.

- But wherever applications entail large scale bespoke engineering – such as construction of a first of a kind nuclear plant, or the retrofitting of carbon capture equipment to an already existing industrial plant, cost reductions have been more difficult or impossible to achieve.

Slide 13

We always knew the theory that learning curve and economy of scale effects could drive down costs: over the last 15 years we have discovered that these are even more powerful than we assumed, but also that they are more likely to apply in some technologies than others.

In addition to technologies where cost reductions are more difficult, there are also sectors where decarbonisation is more difficult – the so-called “hard to abate” sectors: long distance transport, aviation and shipping, and heavy industry, steel, cement and chemicals.

- Battery technology has progressed so fast that even much of heavy duty trucking is likely to be electrified: but we would need currently unforeseeable breakthroughs in battery energy density before we can electrify long distance flight.

- And even if we can electrify the heat input to cement production, we will have to deal with the CO2 emissions resulting from the chemical reaction which turns CaCO3 into CaO.

But even in these so-called hard to abate sectors, the last 5-10 years have seen a revolution in technological possibility and in ambition, and for each of these sectors we now know the technologies that can get us to net-zero: methanol- or ammonia-burning ships, sustainable aviation fuel made from either bioresources or through a synthetic route, and in steel production a range of hydrogen based technologies.

I remember being told only 6 years ago by a major steel company in Japan, that hydrogen direct reduction of iron was an interesting possibility which would be developed in the lab and in small scale pilots in the 2020s, large scale pilots and early demonstration parts in the 2030s and 40s, and might roll out on a large scale between 2050 and to 2070s.

But this is 100g of zero carbon steel made by hydrogen DRI at SSAB’s pilot plant in northern Sweden: and by 2032 SSAB will close all its coking coal blast furnaces. And almost all leading steel companies – from Arcelor Mittal and Tata Steel in Europe and India, to Posco in Korea and Baowu Steel and HBIS in China – are committed to achieving net-zero emissions by 2050 or earlier, with hydrogen likely to play a major role.

In most of these sectors however, there will likely be a significant “green premium” even in the long term;

- In the steel sector it is possible that hydrogen DRI will eventually become a lower cost way of producing iron than using with coking coal blast furnaces.

- But in cement the need to apply CCS means that zero-carbon cement will always be more expensive, however low the cost of electricity.

- And in aviation, it seems certain that the cost of producing sustainable aviation fuel from bio or synthetic sources, will always exceed that of jet fuel produced from fossil fuels. The cost premium will come down over time but it will not be eliminated.

At the business to business level these green cost premia will be significant. So regulation or carbon pricing will be required to drive decarbonisation which will not otherwise occur.

And here, unlike in road transport and/or electrified heating, there will be a some cost increase which consumers will have to bear. But in almost all these hard to abate sectors that consumer cost will be small because the output of these sectors represents only a small cost input to the end product which consumers actually buy.

- If zero carbon steel costs 25% more to produce than carbon intensive steel, the price of an automobile made from zero carbon steel rises less than one percent.

- If shipping freight costs increase 50% because of a switch from heavy fuel to ammonia, the cost of a pair of jeans made in Bangladesh and bought in London will increase by only a trivial amount.

So we have some products and services where once we reach the end state of a zero-carbon economy, consumers will pay lower prices than if we continued with a fossil fuel based one : and others where they will pay slightly higher prices.

And the total gross cost of a zero carbon economy in the end state – the cost which then has to be compared with the benefits of moderating climate change – results from the combination of these positive and negative cost effects.

In his report on the Economics of Climate Change in 2006 Nick Stern suggested that the best estimate cost to achieve by 2050 a 75% reduction in emissions might be 1% of global GDP in that year, in the end state, while the benefits of limiting global warming to 2°C rather than higher might be in a range of 5-20% of GDP and potentially much more.

But Nick’s estimate of 1% of GDP for a 75% reduction now looks a very significant overstatement. In the ETCs report Making Mission Possible, published in 2020, we estimated that the eventual cost to achieve net zero emissions (i.e., a 100% reduction) in the Energy, Building, Industry and Transport sectors of the economy might be only about 0.6%. of GDP. Next year we will pull together a new estimate, and I will be surprised if it is not lower still and potentially even a negative number – indicating a net gain to consumer living standards even before allowing for the huge welfare benefit of moderating future global warming.

Thus over the last 10 to 15 years, reasonable estimates of the eventual cost of living without fossil fuels have significantly reduced: and that’s because of the technological progress and rapid cost production unleashed by learning curve and economy of scale effects in a number of crucial zero-carbon technologies.

The investment challenge

But zero or even negative consumer costs in the eventual state do not mean that getting to a zero carbon economy is costless. There is a cost – the cost of increased investment.

It is an inherent feature of the deeply electrified and decarbonised future economy that the energy system will be more capital intensive: it will entail higher up front capital costs and far lower marginal operating costs.

This capital intensity indeed is what makes the zero carbon economy inherently more sustainable in terms of both its global climate effect and local environmental impacts.

In our current fossil fuel based economy we take out of the ground each year 8000 million tons of coal, 36.5 billion barrels of oil, and 4000 billion cubic metres of gas; we burn them to produce energy and in the next year we have to do the same all over again.

In a zero-carbon economy, we take out of the ground far smaller quantities of materials such as silicon or lithium: we use them to create complex electric structures – solar cells which turn photons into electrons, or cathodes and anodes between which lithium ions flow through an electrolyte. And next year the structures are still largely unchanged and able to perform the same function all over again.

This will be a truly renewable system in a very fundamental sense. But first we have to build it: and that means capital investment.

Capital investment needs

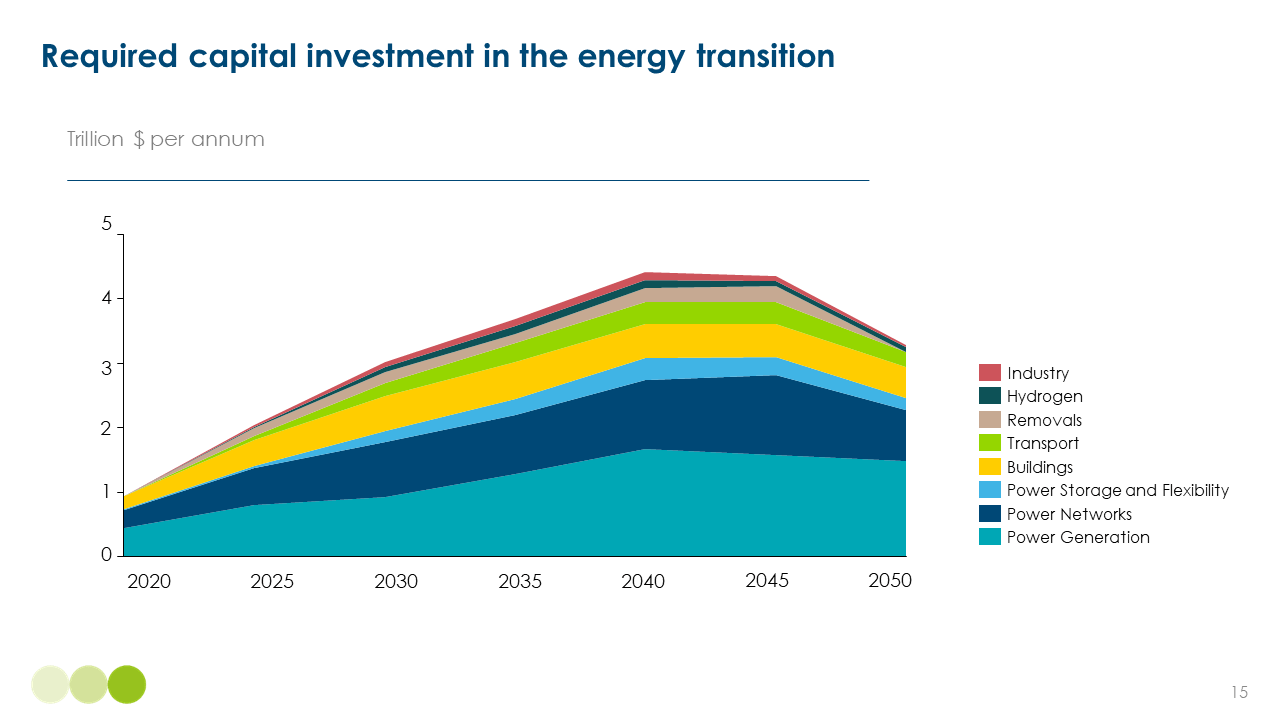

The IEA estimates that investment in the energy, building, industry and transport system will need to rise from around $1.7trillion today to something like $4.0trillion by 2033, partially offset by a full of $0.5 trillion in fossil fuel investment. This is a net increase of around $3.5trillion, which corresponds to about 1.5% of likely global GDP in 2030.

Slide 14

ETC estimates presented in our Financing the Transition report of 2030 are similar, (Slide 14) and show that 70% of that investment is required to build the much larger and zero-carbon electricity systems which lie at the core of any zero-carbon economy – with large investment needs in grids as well as in generation and storage. Investment in buildings to improve energy efficiency is the next most important element.

By contrast investments in industry and long-distance transport – such as new steel mills, CCS installations on cement plants, or ammonia-burning ship engines, are in global terms relatively small, though large relative to individual company resources.

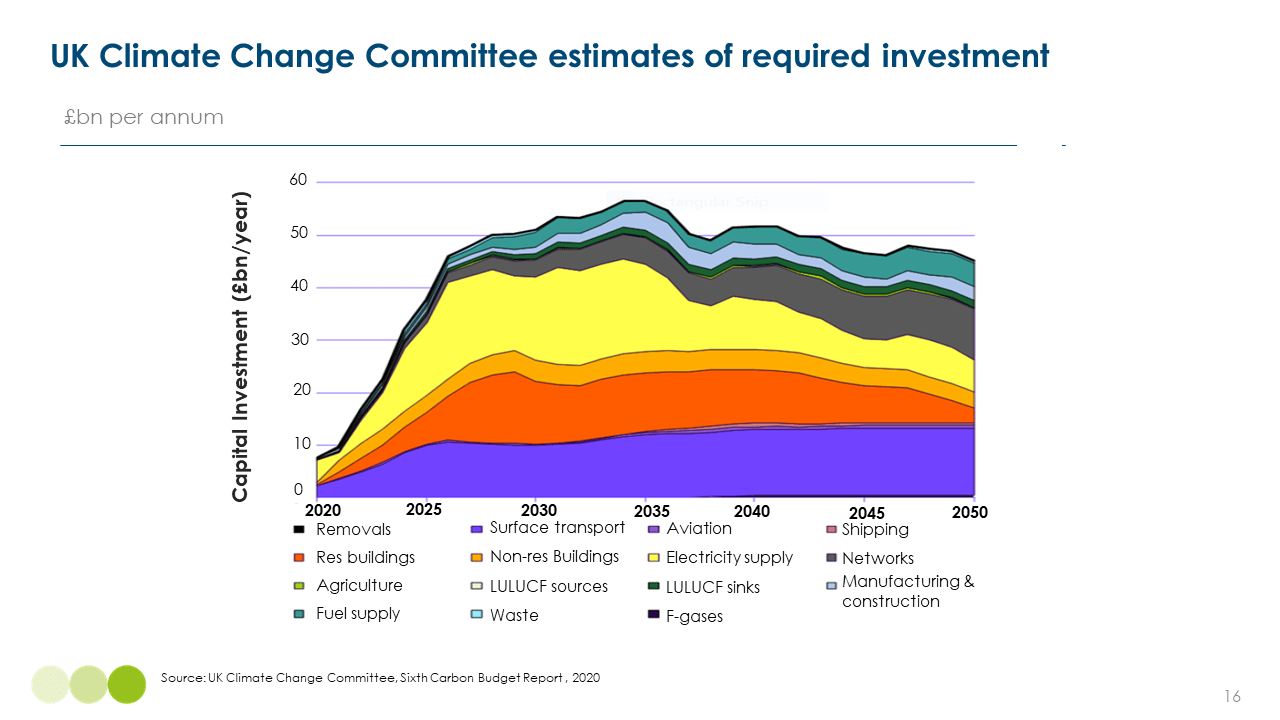

Figures from the UK CCC suggest a similar order of magnitude, with investment in the power system needing to arise to around 1% of GDP by 2030, with another 0.5% in buildings, and with those investment rates maintained over 10 to 15 years before falling in the 2040s as the new system approaches completion (Slide 15).[1]

Slide 15

Slide 16

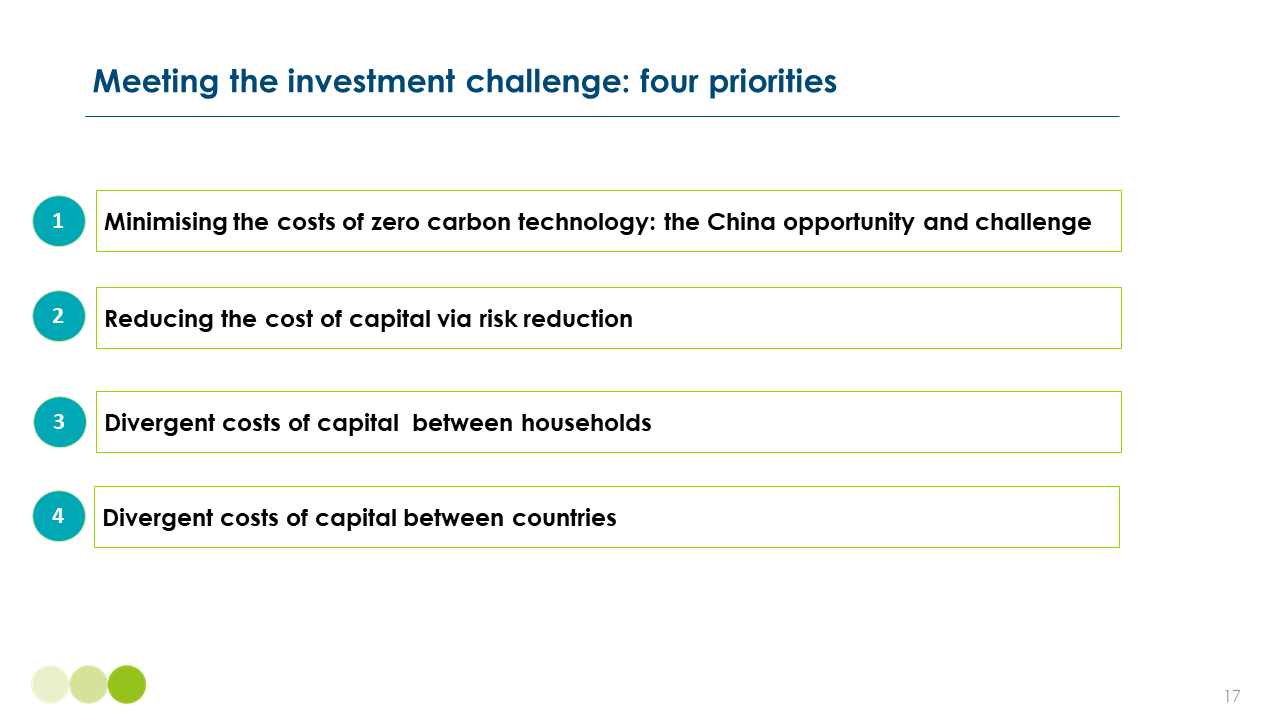

Reducing the cost of capital equipment – the China opportunity and challenge

The first is to ensure that the costs of capital equipment – of solar panels, wind turbines, electrolysers, batteries, EVV and heat pumps – falls as fast as possible.

And here I have earlier told an optimistic story of dramatic reductions in the costs of those core technologies and more to come.

But many of you will have noticed that my examples of rapid progress drew heavily on China.

- It is Chinese companies which have driven solar PV panels down to $.11 per watt.

- Chinese companies now selling high-quality EVs for $10,000.

- And in China that we see dramatic reductions in wind turbine prices.

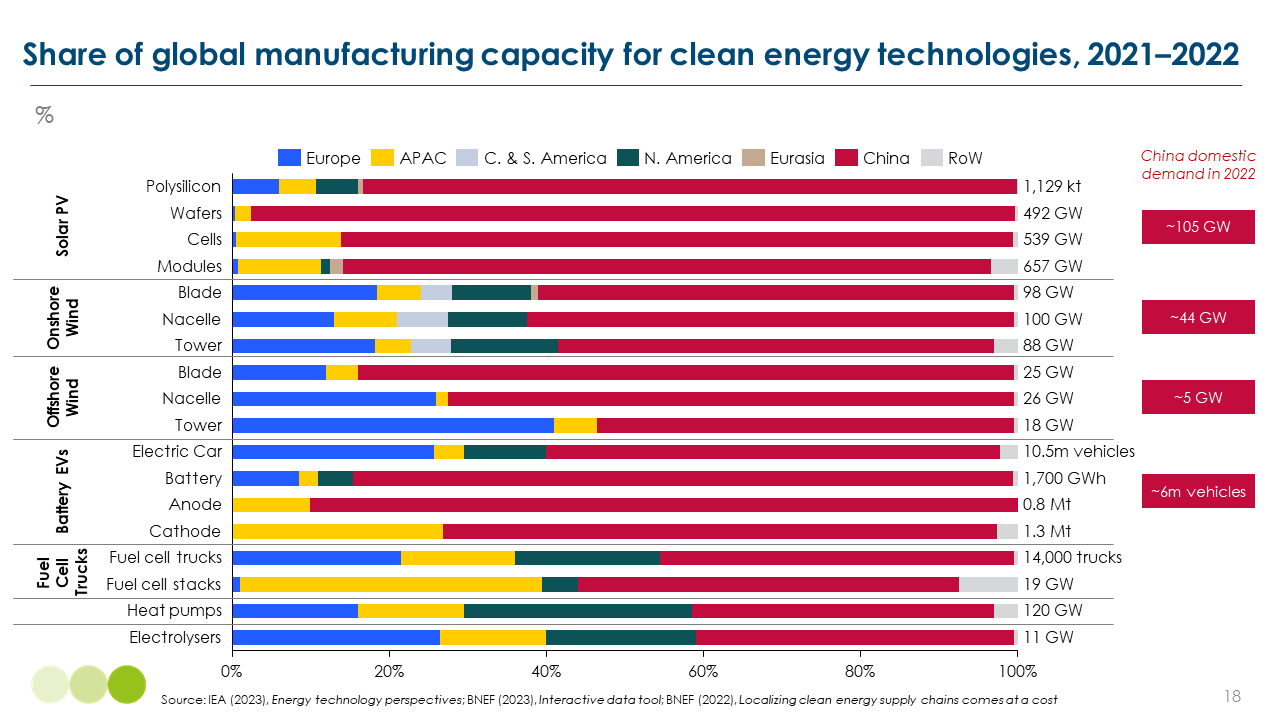

Indeed across almost all the key technologies which will deliver the energy transition to a deeply electrified economy, China currently produces around 80% of global supply (Slide 17).

Slide 17

In an ideal world of peace, political cooperation, and free global flows of technology, trade and capital, this would be no problem: the fact that China can produce solar PV panels for $.11 per watt versus a cost of around 25 to 30 cents in the US would be treated as an opportunity to reduce the costs of solar power.

But in the real world of political and economic competition, and of security concerns, China’s dominance has provoked and was bound to provoke a strong desire to develop domestic supply chains and technological innovation in Europe, the US and India.

The challenge is to ensure that the policies developed in pursuit of that objective speed rather than delay the energy transition, and an ETC report last June set out some of the principles which could help achieve that optimal balance.

In the interest of time I’m not going to go through the details now – but am happy to take questions on them later.

But let me suggest three principles.

- First, optimal policy should primarily focus on time limited subsidies or protection to drive the development of domestic supply chains and innovation which can achieve the same rapid reductions which have been achieved in China.

- Second by contrast, permanently high tariffs could take the pressure off domestic companies to achieve the technological progress and cost reductions which we know are possible. And I note with interest that within the last three months the CEOs of both Mercedes-Benz and Volkswagen have argued against high tariff protection against Chinese car imports.

- Third however – policies such as the European carbon border adjustment, which prevent low cost competition based not on superior technology or scale but simply on lower environmental standards, are entirely justified.

Beyond these three principles there are complex issues to consider; and the ETC will be considering these issues further with our members.

But for the purposes of this lecture, looking back over the last 10 to 15 years, the key message is simple:

- We have seen in that period far faster technological progress and cost reduction than we anticipated and China has played a major role in the progress.

- Even in a world of increased geopolitical tension and competition, we have to find ways to gain global benefits from China’s progress, using it as a stimulus to further innovation and cost reduction across the world.

Reducing risks to cut the cost of capital

Slide 18

The other 3 priorities (Slide 18) relate not to the cost of capital equipment, but to the cost of capital in the financial sense, the cost of debt and the required return on equity.

That cost is influenced by the real risk free rate: and as the ETC’s recent report on offshore wind has illustrated, increases in real risk free rates over the last three years have increased the levelised cost of offshore wind by about $10 per megawatt hour.

But the cost of capital for any specific project also reflects the risk premium which private investors require to cover uncertainties over future costs and revenues.

One crucial risk in renewable energy projects arises from uncertainty about future electricity prices, a risk increased by two inherent features of a renewable electricity system;

- First its close to zero marginal cost of operation.

- And second the intermittency of wind and solar supply, and the resulting potential mismatch between electricity demand and renewable supply.

Together these features mean that any renewable dominated electricity system is likely to see far greater variation in electricity prices across days, weeks and seasons than we have observed in fossil fuel based systems. At times in such a system – when the sun is shining, the wind blowing strongly and demand is low, the marginal price of electricity supply will be zero or even negative: at others it will be very high.

As a result there is a danger that expectations of future prices can be so uncertain that that it is difficult for private investors to justify what at the social level are undoubtedly beneficial investments.

In the theory of rational and efficient markets, there could still be a free market solution to this challenge, with private developers making new investments on the expectation of enormous profits for a small number of hours per year, and/or investing in storage capacity to shift electricity supply from periods of low to high demand. But the inherent complexity and uncertainty of the calculations required in such strategies will increase the cost of capital, and thus the average cost at which power can be supplied in future.

It remains therefore essential for governments to design and participate in markets to reduce the cost of capital for instance through the use of contracts for difference which ensure that developers face a certain fixed price for at least a proportion of their output, while maintaining incentives for innovation in storage, flexibility and demand management.

In the initial development of renewables, before costs had fallen, such contracts also delivered an implicit subsidy, with strike prices set higher than a reasonable expectation of future fossil fuel based electricity prices. But increasingly that subsidy element has disappeared, with two-way contracts as likely to result in payments from developers as to them.

Instead of subsidy, future power market design should concentrate on reducing risks and thus the cost of capital.

And more generally, a crucial objective of public policy in the energy transition should be reduce risk wherever this can be done at low or minimal cost. This requires not only the continued use of CFD or other fix price contracts within power markets but also

- Quantified strategic objectives for the deployment of key technologies – such as offshore wind in the UK – to reduce the risks of supply chain development

- Streamlining planning and permitting systems to reduce uncertainty about how long it will take to deliver projects.

- And well designed regulatory regimes for monopoly private providers of transmission and distribution grids, enabling them to invest ahead of demand.

In addition, there can be an important role for public infrastructure banks even in rich developed countries to absorb risks for which the private sector will charge too high a price.

Variations in the cost of capital by households

Where required investment is primarily financed by companies, the crucial policy objective is to remove risks which unnecessarily increase the cost of capital.

But where investment needs to be driven in part by households, it is also vital to address distributional issues created by the huge variation in the cost of capital between different income groups.

Apart perhaps from agriculture, the biggest challenge which the UK now faces in the path to net-zero emissions is residential heat decarbonization, which will require investment in heat pumps and insulation in some 20 to 25 million households over the next 20 years and ideally earlier.

Delivering that investment is not just a financing challenge – there is also a crucial need to develop the supply chain and workforce skills. But the financial challenge is huge and varies by household type:

- An individual with enough cash in their bank account to sign a cheque for say £15,000 of investment in heat pump and improved insulation, faces an effective marginal cost of capital equal to the rate paid on bank deposits – somewhere around 3.5% nominal.

- But for many middle income people, investment will require taking on more debt, perhaps via increasing their mortgage.

- And for many lower income households the marginal cost of capital is equal to what they would pay on credit cards – 20% or more.

As a result, while richer households may be able to make a reasonable return on heat pump and insulation that investment, for many lower-income households the investment case will often be poor, and policies which require a changeover from gas boilers to heat pumps and do not address this cost of capital issue will provoke political opposition.

Policies to reduce the cost of capital for middle- and lower-income households will therefore be essential;

- In the case of middle-income owner occupiers, one way forward might be for government and the private sector to work together to make additional mortgage borrowing easily accessible at attractively low rates, partly subsidised by government.

- But for lower-income households, direct cash subsidies will likely be needed alongside highly subsidised lending, financed either by taxation, by government borrowing, or via a public investment bank.

Variations in the cost of capital between countries

The cost of capital also varies greatly between different country income groups, and strong international policies will be required to support the energy transition in lower income countries.

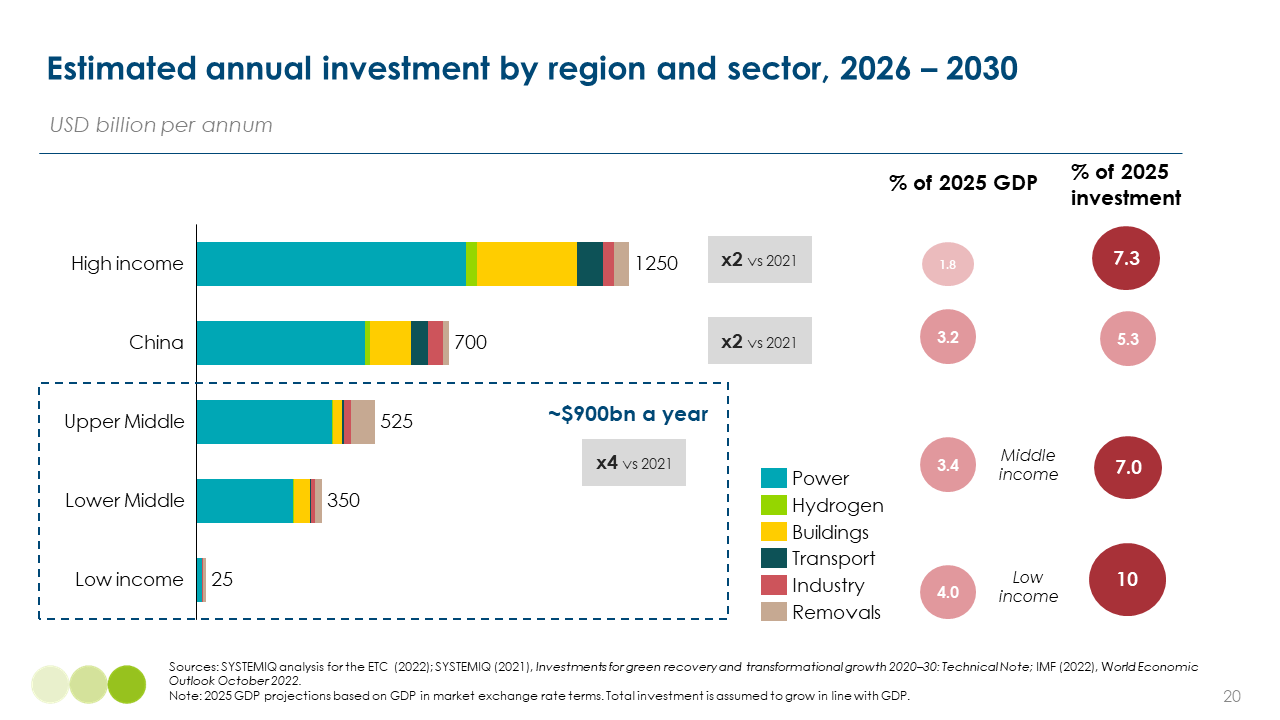

To build a zero-carbon economy will require large increases in investment in countries of all income levels (Slide 19).

Slide 19

From the 2020 level, clean technology investment needs to double by 2030 in the rich developed world and China, quadruple in many upper/middle income countries, but increase five times or more in lower/middle income and lower-income countries.

Up till 2030, absolute investment in lower-income groups will still be small relative to the richer world, but it will need to keep growing in the subsequent 20 years, even as investments in rich developed countries and China plateau and eventually decline.

Since 2020 global investment has already increased dramatically, rising from around $1trillion to $1.7trillion in 2023 according to IEA figures; but so far that increase has been concentrated in the rich developed world, China, and a few middle-income countries such as India, with only minimal growth in low-income countries.

That reflects high perceived risks and a high cost of capital in these countries; a high cost which if not reduced, will greatly delay the potential rapid growth of low-carbon energy systems which technological progress has now made possible.

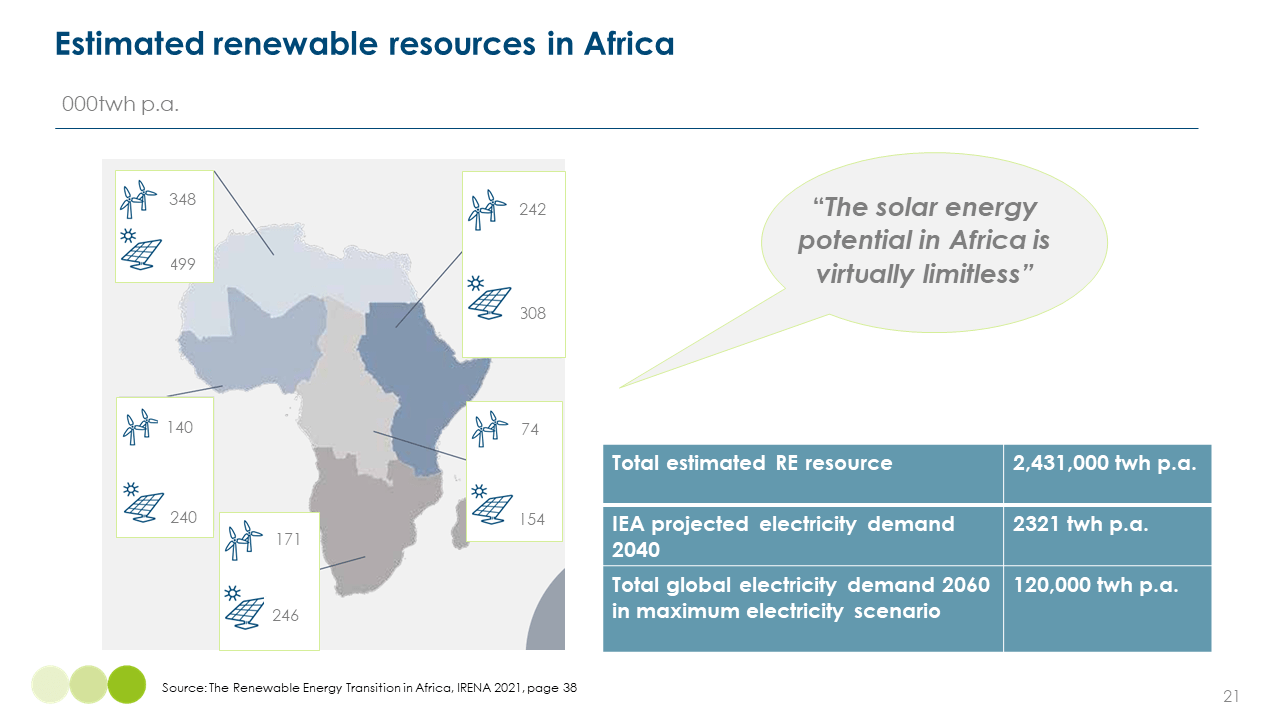

Sub-Saharan Africa, in particular, faces an enormous opportunity to build a far bigger zero-carbon electricity system, largely skipping the phase of fossil fuel development, but can only seize that opportunity if large scale finance for development is available at an adequately low cost.

- It starts with energy per capita use only a 10th of that rich developed countries – and will have to grow energy supply dramatically to support rising living standards for a rapidly growing population. Over the next 40 years, these countries should be aiming to grow electricity supply 10 times or even more.

- And Sub-Saharan Africa is blessed with massive renewable energy resources. IRENA estimates suggest that its technically available wind and solar resource could provide 2.4 million TWh of zero-carbon electricity, some 20 times even the most aggressive forecasts of total global electricity demand in a fully decarbonised economy. As IRENA puts it, “the solar energy potential in Africa is virtually limitless,” (Slide 20).

- It also has the potential, according to IEA estimates, to produce 5000m tonnes of green hydrogen per annum, at locations less than 200km from the coast and at a cost of less than $2 per kilogram. That would be enough to provide 10 times all the green hydrogen that the world will need to decarbonise all its hard to abate sectors.

- Meanwhile the collapsing cost of solar panels – available now at 11 cents per watt, and energy storage batteries (which within 10 years, and perhaps much sooner, will cost well less than $150 per kwh), together with falling wind turbine prices, will make it technologically possible to deliver renewable electricity, round the clock, at costs fully competitive with any fossil fuel based system.

Slide 20

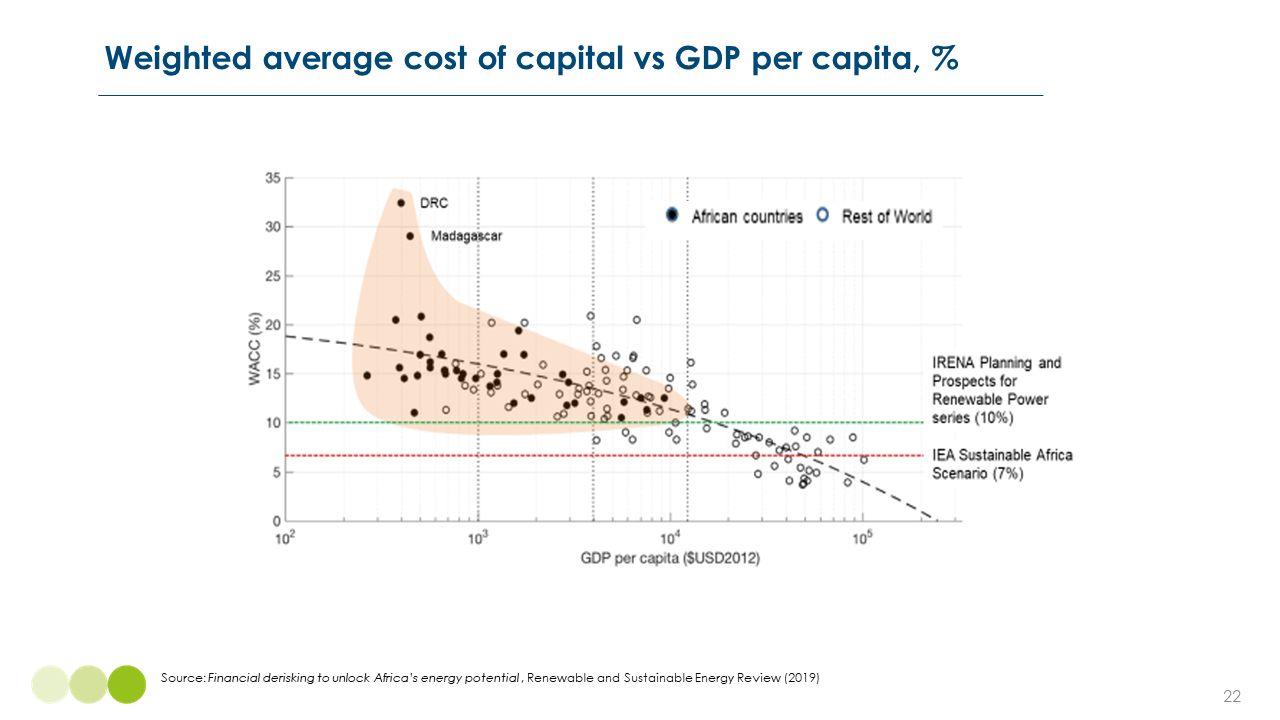

But that potential can only be achieved if finance is available at a lower cost of capital. In a renewable electricity system almost all of the cost is capital expenditure upfront: in a fossil fuel based system the upfront cost is lower but with large operating costs over time. So the relative total cost of renewables versus fossil fuels depends on the cost of capital. If in Sub-Saharan Africa it were possible to build renewable energy systems at the cost of capital available in Europe, the US, let alone in low-cost China, renewables would beat gas turbines hands down. But in many African countries the costs are far higher – an estimated 25% versus 4% percent in Switzerland (Slide 21).

Slide 21

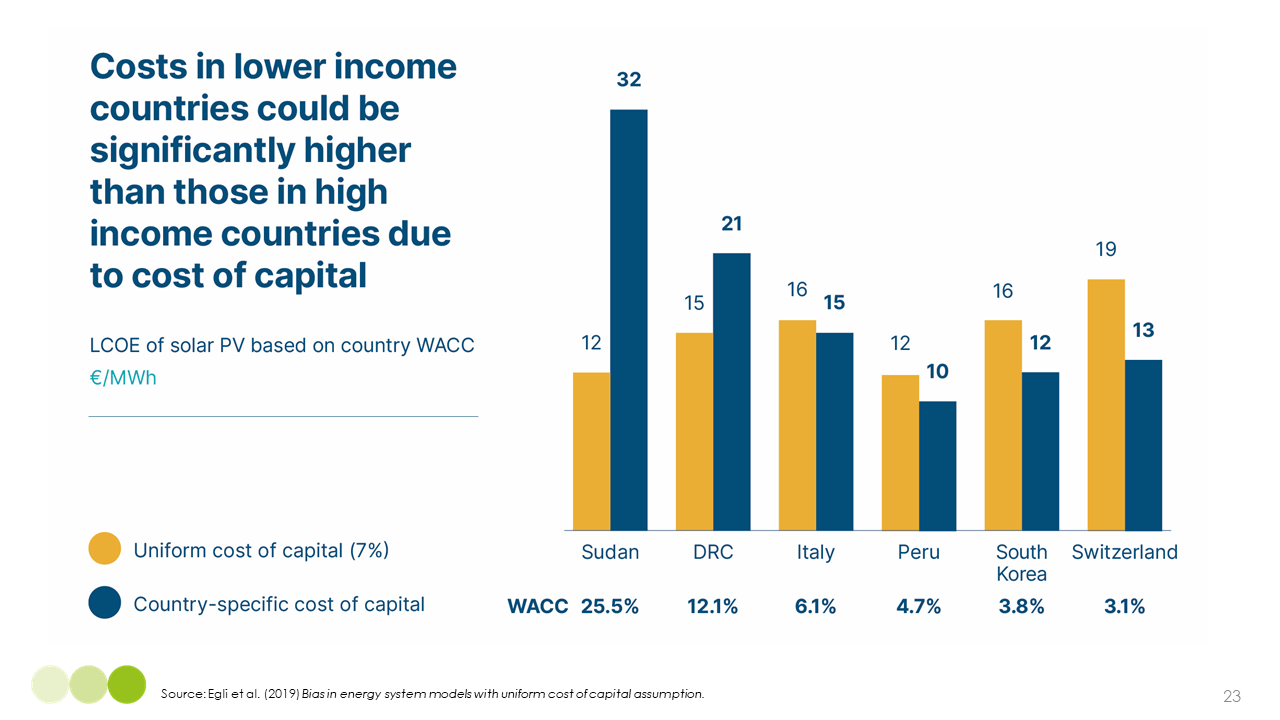

As a result, while Sudan would be one of the cheapest countries in the world in which to produce onshore wind power if it enjoyed a cost of capital similar to those applicable across the world, at its actual costs of capital, its abundant wind and land can only deliver electricity at costs 2 and half times higher than in Switzerland. (Slide 22). At these costs of capital, the logical investment is in a gas turbine, or even just a diesel genset.

Slide 22

The mobilisation of large scale financial flows at a reasonable cost of capital is therefore essential to ensure that developing countries can gain the benefits of the remarkable technological progress we have seen. Over the last 3 years multiple expert reports have set out the scale of the challenge and the actions required to overcome them; increases in the capital resources of the multinational development banks and changes in their lending policies are crucial. Action is now essential to seize the huge opportunity created by technological progress and cost reduction.

Summary – what have we learnt in the last 15 years ?

So let me sum up: what have you learnt about the economics of the energy transition, 10 years on from the start of this lecture series, 16 years on from the launch of the Climate Change Committee. I think six key things:

First, the potential for endogenously induced technological development and for cost reductions deriving from economies of scale and learning curve effects – which we knew about in theory – has practice turned out to be far greater than we dared hope. But this potential is far greater in some specific technologies – mass produced and standardised – than in others – large scale bespoke engineering.

Second, given these trends, the shape of a future zero-emission economy is far clearer than it was 10 to 15 years ago. That economy will be far more electrified than we first thought, and most of the zero carbon electricity to power that economy will come from renewables, even if nuclear and other technologies also play a supporting role.

Third as a result, reasonable estimates of the eventual cost to conventionally measured living standards of shifting to a zero carbon economy are now far lower than when Nick Stern produced his report, or when the Climate Change Committee started work. We thought then that achieving an 80% reduction of emissions by 2050 might reduce UKGDP in that year by 1.5%. It’s now likely that achieving 100% emissions will produce a much smaller impact on living standards and possibly no impact at all.

But, fourth, that does not mean that the transition is costless. The cost is the need to invest to get to the endpoint, and except in some specific circumstances which may not apply, this will mean either less consumption or less investment in other sectors of the economy. Proponents of a zero-carbon economy need to be honest about that cost.

Fifth, it is therefore essential to reduce this investment cost as much as possible in two ways;

- By designing responses to China’s extraordinary technological leadership which help accelerate rather than hold back the cost reductions which we now know are possible.

- And by designing public policies to reduce risks and therefore the financial cost of capital.

Sixth and finally, we have to recognise clearly and respond to the very different costs of capital faced by different households and countries.

Overall I am far more confident than I was in 2008 that at some time in the late 21st century, the world will have a close to zero-carbon economy, delivering clean energy at remarkably low cost to consumers across the world, and with a far smaller adverse impact on the environment than imposed by our fossil fuel system today.

What I don’t know is whether we will get there fast enough to avoid catastrophic climate change.

—————————————————————————————————————————————————————

[1] The CCC figures also show a significant investment in road transport. This reflects an assumption that EVs will continue to be more expensive than ICE vehicles even in the long term. Latest trends in EV prices in China, however, support the ETC assumption that the upfront cost of EVs will fall below cost of ICE vehicles within the 2020s.