Steel

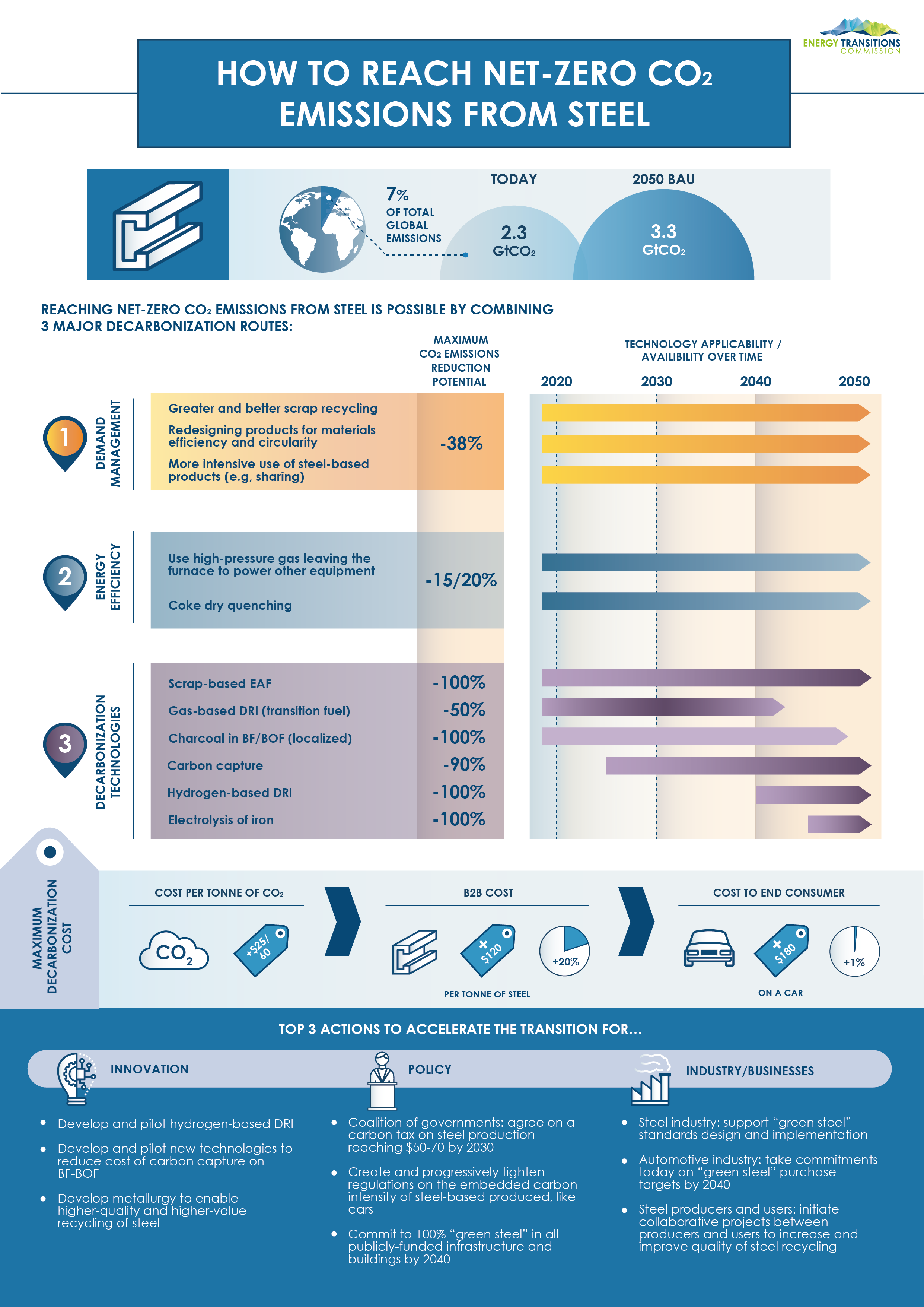

Energy-related emissions from the iron and steel industry currently amount to circa 2.3Gt of CO2, but this could grow to 3.3Gt by 2050 due to demand growth in developing regions. Several technology options could enable decarbonisation of ore-based steel production. In parallel, the development of scrap-based production, which is electrified and lower-emissions, could significantly slow down the growth of ore-based steel demand.

The three main routes to decarbonisation of ore-based production are carbon capture combined with either storage or use (CCS/U), hydrogen-based direct reduction of iron (H2-DRI), or electrolysis of iron. The use of biomass in blast furnaces, technically possible, will be limited due to constraints on sustainable supply of biomass. The optimal pathway will differ by location depending on local resource endowments.

The shift to zero-emissions technologies could increase the cost of steel by about 20%, with minimal impact on end-consumer prices. However, as steel is an internationally traded commodity, an uneven transition on a global scale may create competitiveness issues. Carbon pricing should ideally be applied internationally to drive decarbonisation, but could also be deployed regionally if combined with border carbon tax adjustments.

In the context of the Mission Possible Platform, the ETC convenes and drives the work of the Net-Zero Steel Initiative, which mobilises corporate leadership to shape a favourable policy, market and financing environment that will unlock investment in zero-emissions steel production. The Initiative is currently developing a joint set of policy recommendations, exploring what type of demand signal could really unlock investment in new technologies.

Region publications