This blog underscores ETC Chair, Adair Turner’s speech at Mission 2025’s flagship event, New Economy Rising, which took place during London Climate Action Week 2025. Mission 2025 is a coalition of courageous leaders – mayors, governors, CEOs, investors, citizens – backed by 70+ NGO leaders and organisations, and supported by global real economy giants who are ready to collaborate with governments to support high-ambition COP outcomes and updated national climate plans (NDCs) in line with the Paris Agreement. Adair’s remarks focused on the shifting dynamics of the energy and industrial systems, rising costs of inaction, and the policy and investment levers required to accelerate the shift to a low-carbon economy.

A new set of realities on climate confront businesses and societies in 2025. This year has seen a barrage of economic, political and social headwinds against the energy transition. These are not necessarily signs of failure, but rather evidence that change is underway.

Against these headwinds, the Global Stocktake goals must serve as a guiding star for action and policy. These goals aim to enhance mitigation, adaptation and climate finance support and were last set in 2023 to recalibrate international progress towards the Paris Agreement. They are fundamental to building our economic and societal resilience. The agenda for COP30 this year is shaped by the stocktake goals and marks a critical moment to consolidate national and multilateral commitments towards these shared aims. Meanwhile, the cost of “business as usual” is growing faster than many had feared. In 2024, climate-related damages resulted in losses equal to $320 billion, a one-third increase since 2023; 1 in 5 people around the world feel the impacts of climate change daily; tropical forests were destroyed faster than ever recorded before; and nearly a third of Europe’s river networks flooded. The laws of physics dictate that for every action there is an equal and opposite reaction. If the current trajectory is sustained, these impacts will worsen.

Leaning into the clean energy era

Yet, there are many reasons to remain optimistic. The first half of 2025 has seen strong signals of progress across sectors, indicating a new economy is rising. Prevalence of negative headlines obscures the view over the horizon, but clean technologies are mounting fast.

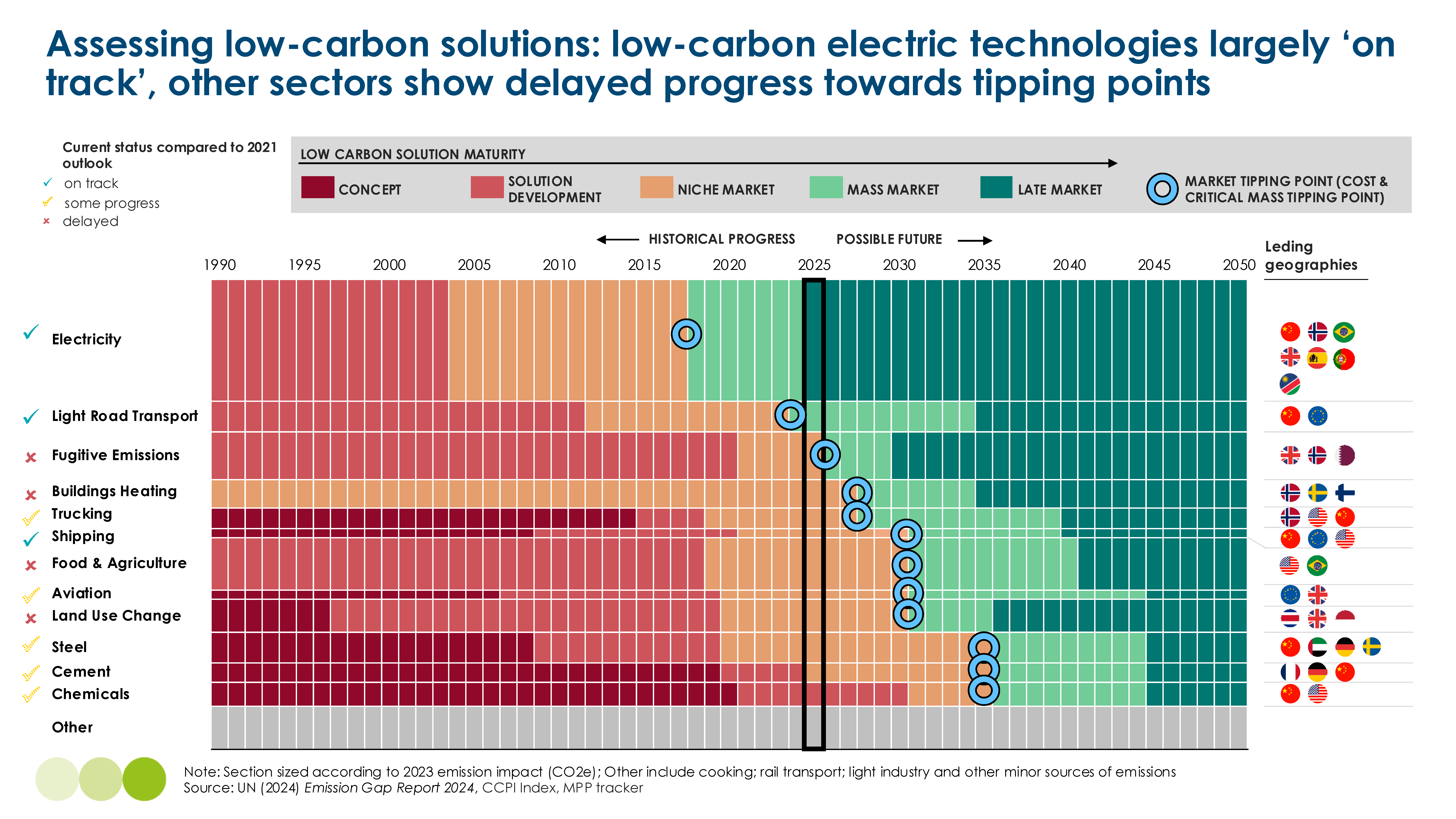

Several key technologies, including solar panels, battery storage and electric vehicles, are already cheaper than fossil-based incumbents and are expected to reach “tipping points” by early 2030 – passing the point of no return as market momentum drives adoption. Also, in the past two years, the cost of solar modules and battery storage systems has halved, meaning each dollar spent buys twice as much. This means that the record levels of clean energy investment reached in 2024 are delivering even more clean energy per $ spent.

These technologies alone could deliver around 40% of the emissions reductions needed to reach net zero, as highlighted in the chart below and new analysis from Systemiq. Furthermore, fossil fuel use is in decline, with coal in retreat and oil nearing its peak, particularly in China where electric vehicles and electrification trends drive substantial reductions in fossil fuel demand.

Clean energy is increasingly displacing fossil fuels. In 2023-2024, new wind and solar generation complemented by 175 GWh of energy storage displaced over 650 TWh of fossil fuel use, saving around $35 billion from being spent on fossil fuels. At the same time, in 2024, greater EV adoption cut oil demand by an additional 0.3 million barrels per day, which is roughly equivalent to powering New York City for half a day, every day. The resulting avoided oil import costs is around $9 billion.

New forces such as artificial intelligence, industrial competitiveness and national energy autonomy are likely to accelerate this shift further as countries look to slash fossil fuel import dependencies for greater energy security. Ember estimates that the deployment of just three key clean technologies: electric vehicles, heat pumps and renewables could reduce net fossil fuel imports by up to 70%.

Breakthroughs in some sectors, bottlenecks in others

However, some industries lag behind, particularly the harder-to-abate sectors such as aviation and heavy industry. Decarbonisation costs remain high and investment decisions are held back by a lack of clear long-term demand signals. These sectors account for around 25% of today’s emissions. Stronger demand signals, supported by policy, could unlock a global pipeline of projects now valued at $1.6 trillion, bringing major economic benefits to host economies.

Although policy progress faces headwinds, some recent multilateral agreements have pulled through, offering a glimmer of hope. For example, the International Maritime Organisation recently passed a global shipping carbon tax backed by China, Brazil, India and 60 other countries; the EU Steel and Metals Action Plan aims to address key competitiveness challenges to the bloc’s metals industry; and the EU Carbon Border Adjustment Mechanism sets a price on imported emissions to the bloc.

Some capital is flowing to nature-based solutions, such as regenerative agriculture and alternative proteins in certain markets, but progress is uneven. For example, Brazil saw $3.6 billion invested in nature-based solutions since 2022. Over 40% of this was mobilised in the last 9 months alone. This momentum needs to be replicated and scaled up across all markets, which may require targeted support and additional resources. This sector contributes around 20% of today’s emissions. Time is running out to make a meaningful impact in this sector by mid-century.

Building economies of the future, today

The energy transition is necessary, desirable, and increasingly within reach. We need to focus this year on key levers across energy, industry, nature, food and finance to stay on course towards the guiding star. The winning economies of the future will be built on cheap solar, wind, batteries and electrification. Renewables and EV deployment are already close to achieving levels required for tripling emissions reductions.

Some critical hurdles remain. At COP28, countries pledged to double energy efficiency and reduce methane emissions, but these are off track towards 2035 targets. Non-energy sectors, such as food and harder-to-abate heavy industry, also remain highly uncertain with current rates of decarbonisation. Nationally Determined Contributions (NDCs) are five year plans which outline country commitments to sector decarbonisation, and could give longer-term clarity needed to unlock investment. COP30 marks the deadline for submitting renewed plans, but only a few countries have submitted so far. Also, many of the NDCs submitted so far are not ambitious enough.

The ambition gap to limit global warming below 1.5°C is significant. Every fraction of a degree counts towards this long-term goal set out in the Paris Agreement. Every fraction of a degree matters to lives and businesses.

What we need now, is to bring the same level of innovation and clarity to climate policy as we are seeing in clean technology. Beyond NDCs, businesses need specific investment-positive policies to light the way. For companies focused on resilience, long-term value, and strategic positioning, now is the time to be specific: what policies do you need to scale climate solutions and shape the rising new economy?