The trajectory to net-zero relies on massive clean electrification: Electricity will grow from 20% of all energy used today to over 60% by 2050. The ETC’s latest scenarios estimate at least a doubling of global electricity use by 2050, potentially reaching over 75,000 TWh compared to today’s approximate 28,000 TWh.1ETC (2023), Fossil Fuels in Transition: Committing to the phase-down of all fossil fuels. To achieve this in just 25 years, the power system must expand in scale and transform how electrons flow through the system.

As world leaders gather for COP29 the Presidency is asking governments, businesses and civil society to sign up to a Grids and Storage pledge which aims to increase global energy storage capacity 6 times above 2022 levels, reaching 1,500 GW by 2030 and to add or refurbish 25 million km of grids. Such commitments can building on COP28’s pledge to triple renewables by 2030, and signal political commitment to accelerate the system-level enablers that are required for rapid renewable deployment.

The rising demand for electricity is led by a shift in power generation (from fossil fuels to renewables) and electrification of end–use sectors such as heating and road transport. Moving to variable renewables like wind and solar leads to a more geographically dispersed generation system, with smaller-scale renewable assets spread across more – and new – locations, with a reduced role for large thermal generation. Massive electrification, with the spread of electric vehicles (EVs), heat pumps, and industrial electrification will often require new or upgraded network connections.

A bigger and more dispersed system of electron flows presents two main challenges:

- The need to build vast amounts of new grids and optimise new and existing grids for maximum efficiency. This includes new wires and transformers, replacing ageing assets, and increasing modernisation (e.g., sensors)) which is one of many tools to increase grid optimisation. Future grids, if highly optimized – through smart power routing, new hardware that reduces losses, and restringing of existing lines – can reduce total build requirements, and increase the efficiency of power flows. Storage and flexibility, as well as the use of long-distance interconnectors, can also lead to a more efficient system. ETC analysis suggests that the size of grids must grow by more than 50% by 2050, growing from around 68 million km of grid in 2023, to a range of around 110–200 million km in 2050.2ETC (2024), Building Grids Faster: The backbone of the energy transition. In addition, the IEA has recently set out a target to build and modernise 25 million km of grids by 2030.3 IEA (2024), From Taking Stock to Taking Action: How to implement the COP28 energy goals.

- The need to manage the system balancing challenge, which arises as the penetration of wind and solar grows, with the need to match electricity demand and supply – from meeting system operation challenges at the fraction-of-a-second level, to providing zero-carbon power around the clock.

Meeting these challenges will require both ‘supply-side’ and ‘demand-side’ routes. Indeed, Supply-side action is critical; the ETC has previously outlined the need to build new grids, and focused on the role of energy storage in short to long durations.

However, the role that demand-side flexibility can play has been previously understated. Demand-side flexibility means being able to shift the consumption of electricity at peak times (e.g. through ‘smart charging’ an electric vehicle, or time-shifting usage of other electricity use), offsetting new grid and generation capacity needed across the system. Traditionally, the power system was based on supply responding to meet growing demand. Modern power systems with higher complexity can be managed with a greater role for ramping up and down demand in response to system needs.

Demand-side flexibility solutions are often cost-effective to deploy and their use is growing, but these can and should scale more rapidly. As electrification accelerates, higher numbers of heat pumps and EVs can provide significant depth for demand flexibility. For example, global EV battery capacity available for grid storage could reach 90–170 TWh by 2050.4Based on 1.7 million EVs in 2050, and a 60-100 kWh average battery pack. Short-term grid storage demand could theoretically be met by EV batteries as early as 2030 across most regions.5Xu et al. (2022), Electric vehicle batteries alone could satisfy short-term grid storage demand by as early as 2030. The use of automated software solutions, which interact with demand-side hardware, are increasing, and will be critical to scaling demand-side flexibility by avoiding the need for direct user action.

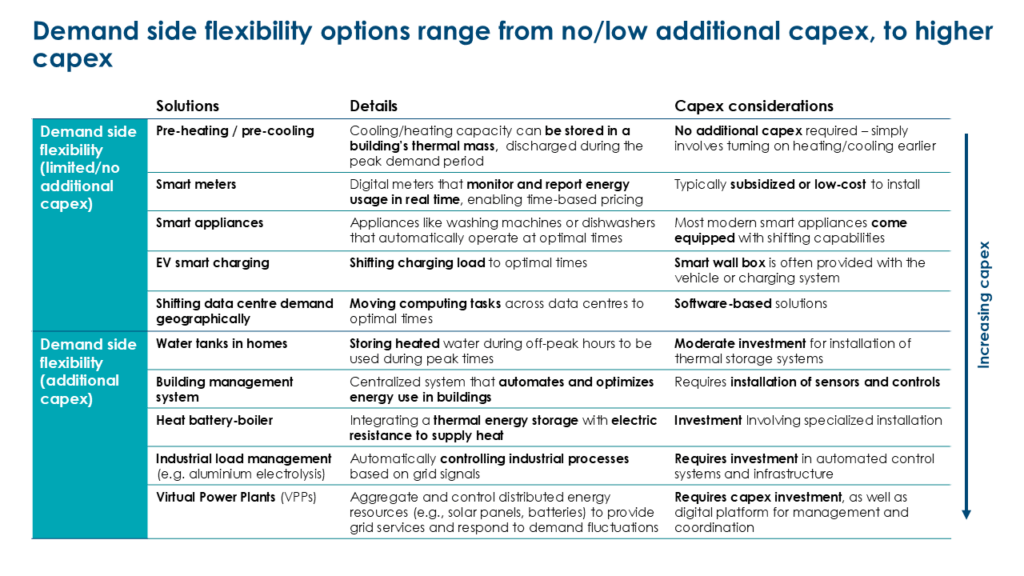

In many cases, demand-side flexibility options are low-cost; many solutions require low to zero additional spend or “capex” (capital expenditure) [Exhibit 1]. For example, heating or cooling buildings a couple of hours ahead of need (“pre-heating” or “pre-cooling”)can be achieved at no additional expense as modern smart appliances are installed with built-in shifting capabilities. Other solutions, such as smart-EV charging are 100% efficient and essentially free to implement – providing a low-cost alternative to short duration storage (such as lithium-ion batteries).6Even on the higher-capex end of the spectrum, research from RMI indicates that virtual power plants (VPPs) that aggregate and coordinate flexible demand can significantly cut power sector costs. By reducing the need for new generation capacity, lowering wholesale energy prices, and deferring transmission and distribution investments, it is estimated that VPPs alone could reduce annual power sector expenditures by up to $17 billion by 2030. See RMI (2023), Virtual Power Plants, Real Benefits.

Exhibit 1: Demand-side flexibility options cost range from zero/low to higher-capex

Demand side flexibility has important potential

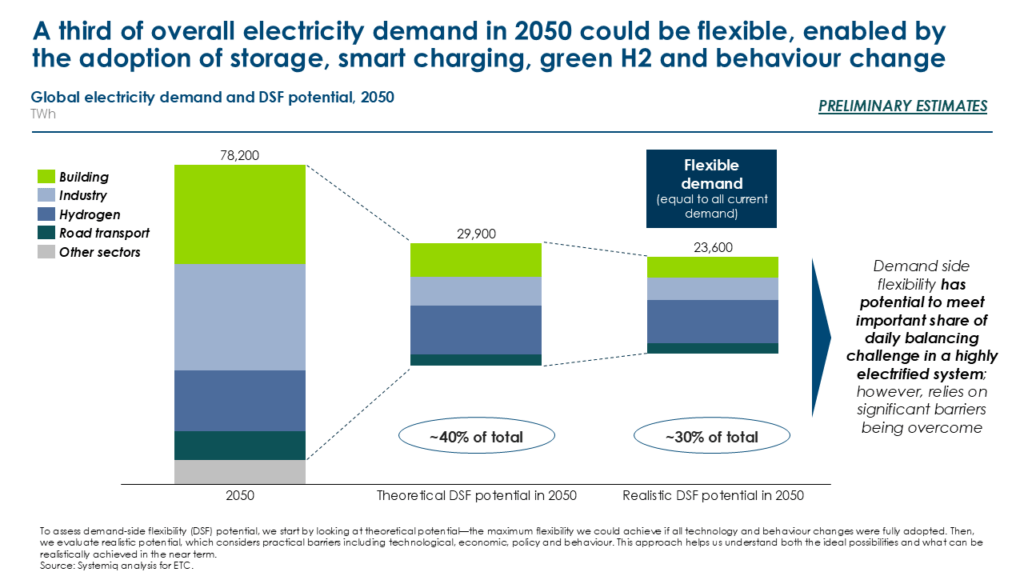

Overall, the ETC’s preliminary analysis suggests that a third of global electricity demand in 2050 could be flexible – roughly equivalent to today’s entire electricity consumption [Exhibit 2]. This flexibility could fundamentally reshape grid dynamics by smoothing peak loads, lowering system costs, and enabling higher shares of renewables.

Exhibit 2: Global electricity demand flexibility potential in 2050

Demand-side flexibility is largely driven by smart technologies and storage solutions. In buildings and industry, thermal energy storage systems can store heat, while battery storage systems provide electricity backup, both of which allow for strategic shifts in energy use. Meanwhile, hydrogen production via electrolysis presents an especially promising flexibility solution. Realising this flexibility potential will require overcoming specific barriers, such as high costs and inadequate regulations.

Furthermore, some uncertainties remain—such as the level of consumer adoption, which depends on user engagement and awareness, as well as potential variations in electrification rates across industry sectors. Additionally, the scalability of certain technologies, like heat battery-boilers, relies on supportive infrastructure and robust market incentives.

Unlocking the potential of demand side flexibility

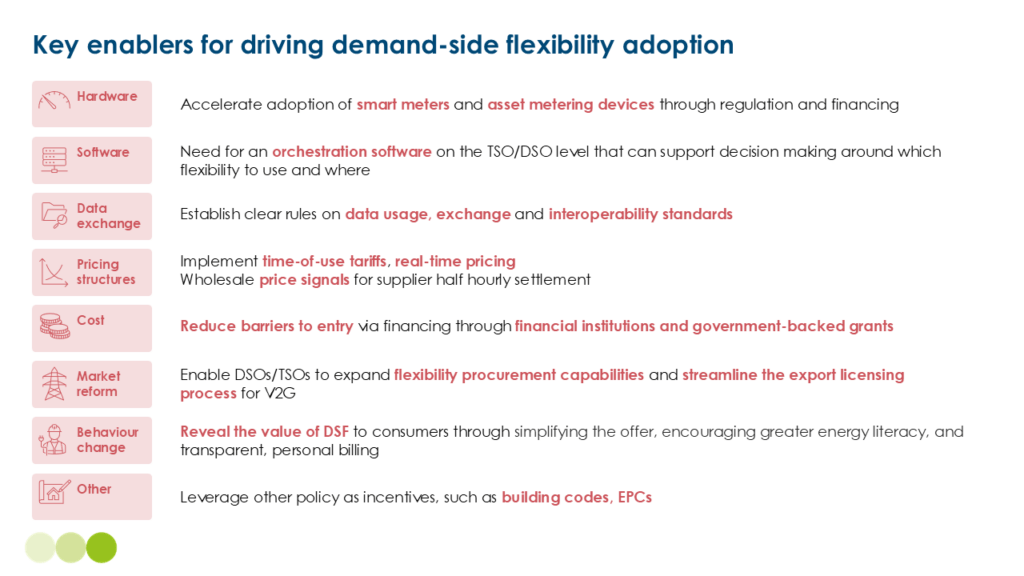

Driving demand-side flexibility adoption at scale requires an integrated approach across several key enablers [Exhibit 3]. Advanced technologies, such as smart meters and energy storage, and intelligent management software and real-time data sharing can enable coordination across the grid. Together, these components allow for dynamic demand adjustments aligned with grid needs, ensuring a responsive and resilient energy system.

Exhibit 3: Key enablers for driving demand-side flexibility adoption

Exhibit 3: Key enablers for driving demand-side flexibility adoption

However, in addition to technical solutions, demand flexibility routes will rely on several other levers. Some of these include:

- Pricing mechanisms, such as time-of-use tariffs. For example, in 2018, Kenya introduced a time of use tariff to encourage large consumers, such as factories, to use electricity during off-peak hours by offering a discount of 50%.7CleanTechnica (2022), Kenya’s Energy Regulator Approves New e-Mobility Specific Electricity Tariffs & New Time of Use Tariffs.

- Market reforms that expand Distribution System Operators (DSOs)/Transmission System Operators’ (TSOs) flexibility procurement capabilities to enhance participation.

- Financial support. For example, Energy Service Companies (ESCOs) can spread capital costs across multiple users and reduce the financial burden on individual customers by bundling and managing demand-side flexibility solutions.

- Behavioural change, as transparency of value, awareness and trust in demand-side flexibility systems can drive wider adoption and lower transaction costs. This is showcased in Hong Kong’s reward point programme, which incentivised consumers to lower load during hot summer evenings that typically spike air conditioning use, in exchange for reward points which could be redeemed for supermarket & food coupons, smart appliances, and more.8CLP (2022), Residential Customers Save 300,000 kWh of Electricity in 4 Hours Responding to CLP’s Energy-Saving Missions in Hot Summer Evenings.

Demand-side flexibility is essential, but only a part of the solution required for a resilient, low-carbon power system. Pursuing new generation and storage capacity additions across the system is crucial. Investments in new grid infrastructure, storage solutions, and long-distance interconnections will remain indispensable to handle the projected demand surges and variable renewable generation. Together, these demand and supply-side approaches can help to deliver the power system of the future.

In 2025, the ETC will be publishing a comprehensive view of routes for optimising power flows, enhancing system resilience, and supporting a clean, electrified future.