This ETC Short reviews the commitments made during the first week of COP26. We will publish an update next week that also includes commitments from week two.

The Paris climate accord committed the world to limit global warming to well below 2°C and ideally to 1.5°C. If we are to keep that possibility of 1.5°C alive and make it certain that we will stay below 2°C, we need not only to head towards a net-zero global economy by mid-century but make big emissions reductions in the 2020s.

Ahead of this COP we at the Energy Transitions Commission set out six sets of actions which could build on NDCs to achieve the reductions required, set out in our report Keeping 1.5°C Alive: Closing the gap in the 2020s. The report highlighted technical and economically feasible actions which, if realised, would reduce carbon dioxide (CO2) emissions by around 45% and methane (CH4) emissions by 40% by 2030, putting a 1.5°C pathway within reach.

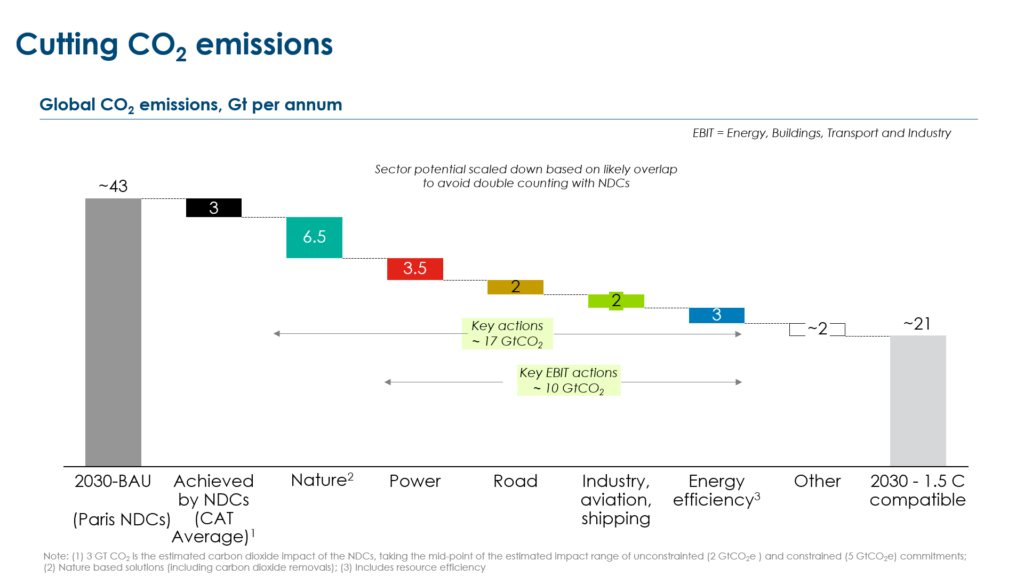

On a business-as-usual pathway global CO2 emissions could reach ~43 GtCO2 in 2030. If we are to maintain a pathway which is consistent with limiting temperature increase to 1.5°C global emissions will need to fall by ~22 GtCO2/year by 2030, alongside a ~150 Mt/year reduction in methane. Of the 22 GtCO2/year gap, only ~3 GtCO2/year in reductions was pledged in national commitments (Nationally Determined Contributions) made by October of this year, taking a mid-point of unconditional and conditional national pledges (ETC estimated a further 20 MtCH4 are included in NDCs, equivalent to 0.5 GtCO2e if using a 100-year multiplier).13 Gt CO2 is the estimated carbon dioxide impact of the NDCs, taking the mid-point of the estimated impact range of unconditional (2 GtCO2e) and conditional (5 GtCO2e) commitments from Climate Action Tracker’s Emissions Gap estimates as of September 2021. Although further NDCs have been announced during COP26 (e.g. from India), we have not attempted to account for this in this analysis.

Beyond NDCs, we estimate ~17 GtCO2/year of feasible emissions reduction potential could be achieved in the 2020s, with an additional 6.6 GtCO2 of reductions delivered by “Nature-Based Solutions” and ~10 GtCO2 via accelerated reduction of emissions from the energy, building, industry and transport sectors (Figure 1). These emissions reductions estimates are scaled down in order to try to avoid double-counting with actions already included in NDCs.2The ETC approach in this analysis was the same for our Keeping 1.5C Alive report, where we scaled back the additional impact of action in the 2020s to try to account for what is already included in NDCs, recognizing that quantifying what is included in NDCs for each sets of actions is challenging. Although this is not an exact science, we believe most double counting between the announcements and the NDCs is avoided. Further detail on our methodology can be found on p28 of the main report and p15 of the technical annex found here: https://www.energy-transitions.org/publications/keeping-1-5-alive/

Each additional action in the 2020s has been scaled back according the following factors:

Nature based solutions (incl. Carbon removals): Assumed 10-15% of action is already covered in NDCs

Decarbonising the power sector: Assumed 20-30% of action is already covered in NDCs

Decarbonising road transport: Assumed 10-15% of action is already covered in NDCs

Supply-side decarbonisation in other sectors: Assumed 5% of action is already covered in NDCs

Energy and resource efficiency: Assumed 10-15% of action is already covered in NDCs

If these savings can be delivered in addition to existing commitments within the NDCs we can in principle close over 90% of the gap between a business-as-usual scenario and a 1.5°C aligned trajectory. These commitments at COP26 complement existing NDC commitments, focusing on the highest potential areas for short-term action, and can generate the momentum for future reinforcement of NDCs over the next two years (e.g. by the global stocktake in 2023).

Figure 1: Key actions required to reduce CO2 emissions in 2030

Source: Energy Transition Commission “Keeping 1.5oC Alive” (2021)

The question after one week of COP and many new commitments is, how close are we to closing the gap?

The first week of COP26 saw a flurry of announcements and headlines across a range of issues. Key agreements were unveiled in multiple areas – including methane, nature and coal – to varying degrees of specificity and tangibility. Equally varied were the lists of signatories; although all of the policy agreements contained backing from several big economies, each also had notable absences.

This ETC Short reviews the commitments agreed upon last week, and assesses how much of the emissions gap could be covered by announcements made during week 1 of COP26, if these announcements are then fully delivered in the next decade.

Methane

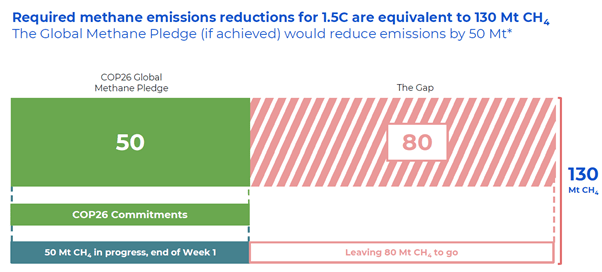

In Keeping 1.5°C Alive, . On Tuesday last week more than 100 countries joined the US and EU in committing to the Global Methane Pledge, which seeks to reduce CH4 emissions by 30% by 2030, relative to 2018 levels. The countries signed up to the pledge account for ~45% of global CH4 emissions today.

Summary impact: If each of the signatories succeeds in reducing their own methane emissions by 30%, total annual emissions would decline by ~48 MtCH4.3Russia and Iran are large methane emitters given their gas production and reliance on very old, leaky gas transmission infrastructure. China is the world’s number one CH4 emitter, owing to its rice paddies and coal mines. The US is also a large methane emitter, and a 30% reduction in US methane emissions would reduce CH4 emissions by around 9 Mt. Whilst no explicit detail on methane reductions was included in the US’s April NDC, further details have recently been stated in the recent Long-term Strategy Methane Emissions Reduction Action Plan, suggesting a reduction of up to 8 MtCH4 could be possible by 2030. That is a good start but falls short of the 130 MtCH4 potential identified by the ETC in Keeping 1.5°C Alive. In part this shortfall reflects the absence of some of the world’s largest methane emitters, including Russia, China and Iran.

Nature

The ETC estimates that emissions from deforestation, coastal and peatland degradation could be reduced by 4.6 GtCO2/year by 2030 (3.6 Gt from avoiding deforestation and 1.0 Gt from avoiding coastal and peatland degradation). Week 1’s “Nature Day” saw more than 100 countries – including large deforesters such as Brazil and Indonesia – sign up to the Leaders declaration on Food and Land Use (FLU), which pledged to end deforestation by 2030, accounting for ~85% of the world’s forests. This was supported by a FACT dialogue statement signed by multiple countries supporting increased supply chain transparency, with a view to avoiding deforestation.4Forests, Agriculture and Commodity Trade dialogue. See: https://ukcop26.org/forests-agriculture-and-commodity-trade-a-roadmap-for-action/

However, a similar pledge was also put forward in 2014, and deforestation rates have increased since then. Similarly, the ETC’s Keeping 1.5°C Alive report suggested that achieving the full 4.6 GtCO2/year savings by 2030 could require up to US$200bn per year in finance, but the funding committed behind these pledges falls far short of this (currently at less than $15bn, spread over the next four years). Furthermore the statement does not detail how the implementation of the agreement would be tracked, or what might happen if nations renege on the promise. While the commitment itself is a step forward, delivering it – including the required finance – is a huge priority. If delivered, we estimate this pledge could cut emissions by an additional ~4.0 GtCO2/year by 2030.

In addition to deforestation, a total of 45 nations signed on to a new Policy Action Agenda, designed to help policymakers deliver the necessary changes to agriculture (amongst other agricultural initiatives). However as this was not accompanied by specific targets or actions, we have not been able to estimate the impact of these agriculture announcements on emissions reductions.

Summary impact: After scaling down our estimated impact of avoiding emissions from deforestation to account for double-counting in NDCs, we estimate total potential savings in 2030 from Nature could, if delivered, reduce emissions by around 3.5 GtCO2/year in 2030.5Of this, avoiding deforestation in Brazil and Indonesia account for around 0.8 GtCO2/year and 0.5 GtCO2/year respectively. CAT estimates suggest NDCs in these countries account for, at most, up to 0.2 GtCO2/year of emissions reductions.

Coal and power sector decarbonisation

The ETC’s Keeping 1.5°C Alive report estimated that 3.6 GtCO2/year could be avoided from coal power generation in 2030: 0.7 GtCO2 from no further construction of coal fired power plants, 1.2 GtCO2 from phasing out existing coal in OECD by 2030, and a further 2.3 GtCO2 from early phase-out of older generation in non-OECD countries.

Last week’s Global Coal to Clean Power Transition Statement saw more than 40 countries commit to ending all investment into new coal power generation domestically and internationally. Signatories from developed economies also pledged to phase out coal power in the 2030s whilst emerging economies would phase out during the 2040s.

Although this provides some signals that “the end of coal is in sight” there are several major caveats to note:

- First, the phase out dates may not be as ambitious as is required for a 1.5°C pathway. Keeping 1.5°C Alive (and other similar reports including the IEA Net Zero Report) notes the need for coal to be phased out by 2030 for advanced economies (2040 for Rest of World), not during this decade. The deadlines in the current statement are around 10 years behind this.

- Second, the list of signatories was a mixed bag. New commitments from large and growing Asian emitters Vietnam and South Korea were a welcome surprise to many observers. Indonesia’s pledge came with the stipulation that the country will finish building some new coal plants before its stopping altogether, but this still represents significant progress from even one year ago.

- Less encouragingly, Poland, signed up but made clear its target date for final phase out is 2049 – no different from its existing timeline. And of course missing were both China and India, neither of which signed up to the statement but account for the vast majority of the new coal pipeline, and large volumes of existing coal.

Together therefore, we estimate the impact of this initiative at just 0.2 GtCO2/year in 2030.

However other initiatives that focus on the power sector provide confidence that further emissions reductions could be possible here. For example, further signatories signed up to the Powering Past Coal Alliance – a group of countries, sub-national entities and businesses focusing on the phase-out of existing coal, a crucial priority if we are to meet 2030 targets – the Race to Zero6The Race to Zero campaign aims to accelerate private sector action on climate. Each Race to Zero breakthrough is gaining agreement on ‘Breakthrough ambitions’ from a critical mass of companies in each sector. These ambitions are expected to scale over time, in order to achieve longer-term outcomes (2030 targets) and goals (beyond 2030). So far ‘breakthrough ambition’ has been achieved in 17 sectors, with more announcements expected soon. Where the Race to Zero breakthroughs overlap with the ETC’s analysis, we were able to estimate the impact of the agreed ‘breakthrough ambitions’, based on the assumption that the agreed ambitions – announced by ~20% of companies within specific sectors – are able to lead to the suggested outcomes in 2030. commitments from businesses to scale up renewables (see below), and the innovative South Africa coal finance deal.7Although South Africa didn’t sign up to the Coal-to-Clean transition statement, the start of its phase-out supported by several western states was announced earlier in the week, highlighting the importance of climate finance in delivering an early exit from coal (as noted in the Keeping 1.5C Alive report). If the ambition underlying these initiatives were fully delivered by 2030, we estimate this could add a further 1.5 GtCO2/year of emissions savings.

Summary impact: Our estimate suggest that commitments to no new coal will reduce emissions by just ~0.2 GtCO2; just ~5% of the potential we assessed in our report, due to the absence of big emitters such as China and India. However further initiatives in the power sector have the potential to deliver a further 1 GtCO2/year of emissions reductions in 2030, if fully implemented. Accounting for the potential impact that is likely included in existing NDCs, these commitments could add 1.2 GtCO2/year beyond current NDCs.

Road Transport

The ETC’s Keeping 1.5°C Alive report identifies ~2.6 Gt of potential CO2 savings in the road transport sector by 2030. Driving this is a ban on all sales of ICE light-duty vehicles by 2035, combined with city-based action to restrict the use of existing ICE vehicles beyond defined future dates. Together these could lead to around 20% of cars on the road being electric by 2030 and deliver around 2 GtCO2/year of reductions. An additional 0.6 GtCO2/year of savings could be possible improved heavy-duty truck efficiency.

Summary impact: Our estimates suggest that the commitments to electrification already made by auto manufacturers – whether within the Race to Zero framework or outside of it – alongside country commitments to end the sales of fossil fuelled vehicles imply that road transport electrification for light-duty vehicles will go much faster than most NDCs assume. This will likely deliver an additional 1.5 GtCO2 beyond NDCs in 2030 (after scaling back to avoid double-counting). Ideally, this will also be recognised in country commitments at COP26.

Other initiatives announced in the past week

Four major economies – Australia, Indonesia, Japan and Nigeria – signed onto the Product Efficiency Action Plan, aimed at rapidly improving the energy efficiency of products sold around the world. This brings the total number of signatories to 14, covering approximately 50% of the total emissions reduction potential. The plan sets out to double the efficiency by 2030 of products in four key areas: lighting, refrigerators, air conditioners and industrial motor systems – which together account for over 40% of global electricity demand.

Countries representing ~70% of global GDP signed up to the “Breakthrough Agenda” which seeks to reduce the cost of clean technologies by 2030 in four key sectors: power, road transport, steel production and hydrogen. The COP parties also committed to develop global metrics to enable tracking of progress of both state and non-state initiatives, led by the IEA, IRENA and HLC in collaboration with other international initiatives (including Net Zero Steel Initiative for Steel).

Lastly, Mark Carney unveiled the Glasgow Financial Alliance for Net Zero (or GFANZ) – a global coalition of leading financial institutions committed to accelerating the decarbonization of the economy. The purpose of GFANZ is to hold the financial community accountable for its pivotal role in addressing climate change. It is made up of 450 institutions from around the world that have $130 trillion worth of assets under management – the ambition is to align these assets with Net Zero commitments.

Though these initiatives support the sector initiatives identified above, we haven’t included any specific quantification of these initiatives.

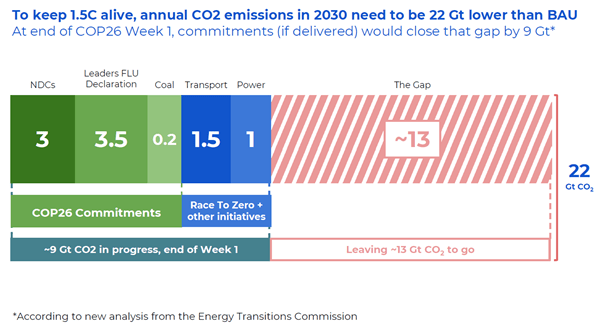

Summary of week one: 9 Gt in progress and to be delivered, 13 Gt to go

Taken together, existing NDCs are likely to contribute around 3 GtCO2/year to the 22 GtCO2/year emissions reduction gap in 2030 – 15% of the gap.

If delivered, we estimate the sector initiatives announced at COP to date could add a further ~6 GtCO2/year of emissions reductions in 2030 beyond NDCs. This estimate includes:

- The COP26 sector initiatives announcements: representing an additional 3.7 GtCO2 – 15% of the gap

- 3.5 GtCO2 from leaders declaration on Forestry and Land Use,

- 0.2 GtCO2 from the Global Coal to Clean Power Transition Statement

- Country, company and financial sector commitments,8This includes commitments from companies in key sectors that will deliver emissions reductions announced before Glasgow, but which were not considered as part of the Energy Transition’s analysis in September estimating a 22 GtCO2 gap. This reflects that changes in the real economy are accelerating action on climate change beyond country NDCs. including those made as part of Race to Zero have the potential to deliver an additional 2.6 GtCO2 – 10% of the gap

Additional commitments made at COP26 to date are important steps in the right direction, but will require additional finance and committed action from public and private sector parties in order to be successfully delivered.

Together these actions can close around 40% of the gap between a business-as-usual scenario in 2030, and a 1.5°C consistent pathway. Recognising this, parties should build on the momentum across public and private sectors and update NDCs to reflect the additional progress agreed through initiatives at COP26.

What to expect next

This week, negotiations are continuing on the Article 6 rulebook (potentially opening the doorway to an international carbon market mechanism), loss and damage, and other critical issues. Further sector announcements are also expected. Overall, countries will work towards a final COP cover decision by the end of the week.

The goal over the coming week should be to ensure that the final COP decision text recognises these initiatives, and acknowledges that these additional opportunities should be reflected in future, tightened NDCs in the coming years (e.g. by the 2023 global stocktake). If the commitments described here are integrated into future NDCs, with savings delivered in addition to current NDCs in the 2020s, they can take us some way to keeping alive the potential to limit global warming to 1.5°C.

Taken together, good progress has been made, but is still not enough and even with further progress next week – on steel, aviation, shipping – we are not going to achieve the full 22 gigatons we need; we’re not going to be able to go home from Glasgow saying job done.

But we have new commitments which will make a difference and which must be delivered, and we have a springboard for further progress which we must achieve over the next few years sector by sector, and country by country, and reflect in improved NDCs.

Technical Notes

[1] 3 Gt CO2 is the estimated carbon dioxide impact of the NDCs, taking the mid-point of the estimated impact range of unconditional (2 GtCO2e) and conditional (5 GtCO2e) commitments from Climate Action Tracker’s Emissions Gap estimates as of September 2021. Although further NDCs have been announced during COP26 (e.g. from India), we have not attempted to account for this in this analysis.

[2] The ETC approach in this analysis was the same for our Keeping 1.5C Alive report, where we scaled back the additional impact of action in the 2020s to try to account for what is already included in NDCs, recognizing that quantifying what is included in NDCs for each sets of actions is challenging. Although this is not an exact science, we believe most double counting between the announcements and the NDCs is avoided. Further detail on our methodology can be found on p28 of the main report and p15 of the technical annex found here: https://www.energy-transitions.org/publications/keeping-1-5-alive/

Each additional action in the 2020s has been scaled back according the following factors:

- Nature based solutions (incl. Carbon removals): Assumed 10-15% of action is already covered in NDCs

- Decarbonising the power sector: Assumed 20-30% of action is already covered in NDCs

- Decarbonising road transport: Assumed 10-15% of action is already covered in NDCs

- Supply-side decarbonisation in other sectors: Assumed 5% of action is already covered in NDCs

- Energy and resource efficiency: Assumed 10-15% of action is already covered in NDCs

[3] Russia and Iran are large methane emitters given their gas production and reliance on very old, leaky gas transmission infrastructure. China is the world’s number one CH4 emitter, owing to its rice paddies and coal mines. The US is also a large methane emitter, and a 30% reduction in US methane emissions would reduce CH4 emissions by around 9 Mt. Whilst no explicit detail on methane reductions was included in the US’s April NDC, further details have recently been stated in the recent Long-term Strategy Methane Emissions Reduction Action Plan, suggesting a reduction of up to 8 MtCH4 could be possible by 2030.

[4] Forests, Agriculture and Commodity Trade dialogue. See: https://ukcop26.org/forests-agriculture-and-commodity-trade-a-roadmap-for-action/

[5] Of this, avoiding deforestation in Brazil and Indonesia account for around 0.8 GtCO2/year and 0.5 GtCO2/year respectively. CAT estimates suggest NDCs in these countries account for, at most, up to 0.2 GtCO2/year of emissions reductions.

[6] The Race to Zero campaign aims to accelerate private sector action on climate. Each Race to Zero breakthrough is gaining agreement on ‘Breakthrough ambitions’ from a critical mass of companies in each sector. These ambitions are expected to scale over time, in order to achieve longer-term outcomes (2030 targets) and goals (beyond 2030). So far ‘breakthrough ambition’ has been achieved in 17 sectors, with more announcements expected soon. Where the Race to Zero breakthroughs overlap with the ETC’s analysis, we were able to estimate the impact of the agreed ‘breakthrough ambitions’, based on the assumption that the agreed ambitions – announced by ~20% of companies within specific sectors – are able to lead to the suggested outcomes in 2030.

[7] Although South Africa didn’t sign up to the Coal-to-Clean transition statement, the start of its phase-out supported by several western states was announced earlier in the week, highlighting the importance of climate finance in delivering an early exit from coal (as noted in the Keeping 1.5C Alive report).

[8] This includes commitments from companies in key sectors that will deliver emissions reductions announced before Glasgow, but which were not considered as part of the Energy Transition’s analysis in September estimating a 22 GtCO2 gap. This reflects that changes in the real economy are accelerating action on climate change beyond country NDCs.